Kuroda Haruhiko published a long article on monetary policy: insisting on easing to boost the economy does not require a choice between the economy and inflation

Kuroda Haruhiko believes that Japan’s economy is still recovering under the haze of the epidemic, and its income is also under downward pressure from rising commodity prices, and it does not have the conditions to tighten monetary policy at all. Furthermore, the Bank of Japan does not face a trade-off between economic stability and price stability, and is therefore well-positioned to continue stimulating aggregate demand from a monetary perspective.

On June 6, the Governor of the Bank of Japan Haruhiko Kuroda published an article entitled “The Concept of Monetary Policy – Towards the Sustainable and Stable Realization of the “Price Stability Goal”, expounding the Bank of Japan’s thinking on the country’s current monetary policy.

Kuroda Haruhiko believes that Japan’s economy is still recovering under the haze of the epidemic, and its income is also under downward pressure from rising commodity prices, and it does not have the conditions to tighten monetary policy at all.

Therefore, the top priority for the BOJ right now is to firmly support economic activity by persevering in maintaining a strong monetary easing policy on the basis of current yield curve control.

Kuroda also said that unlike foreign central banks, the Bank of Japan does not face a trade-off between economic stability and price stability, and is therefore well-positioned to continue stimulating aggregate demand from a monetary perspective.

The following is the full text translation:

1 Introduction

In March last year, the Bank of Japan had just completed its “assessment” in order to increase the sustainability and flexibility of monetary easing, and that’s when I realized the long-term effects of the new crown epidemic. After that, under the reopening of the world‘s economic activities, the conflict between Russia and Ukraine broke out, and the price situation at home and abroad has undergone tremendous changes. In particular, the speed of inflation has far exceeded the expectations of many experts in Europe and the United States. Recently, the Federal Reserve officially began to reduce monetary easing. In addition, although Japan’s consumer prices are lower than those in Europe and the United States, in April this year, Japan’s CPI increased by more than 2% year-on-year, the first time since the summer of 2008. Even under these circumstances, the Bank of Japan has made clear its stance on continued strong easing of monetary policy, unlike its European and American counterparts.

Today, I will intersperse and compare the situation in Europe and the United States to talk about why it is necessary for my country to continue to maintain monetary easing. In addition, I would like to share my views on how the Bank of Japan can achieve its “price stability objective” stably and sustainably.

2. Views on the current implementation of monetary policy

Basic view of monetary policy execution based on economic and price conditions

First, let me talk about the basic views on the current execution of monetary policy. The Bank of Japan needs to maintain a strong monetary easing policy for three reasons.

First, my country’s economy is still trapped by the epidemic and is in the process of recovery.Unlike Europe and the United States, Japan’s real GDP has so far failed to return to pre-pandemic levels (Figure 1). From January to March this year, due to the prolonged supply bottlenecks such as semiconductors and components, as well as the pressure on service consumption brought about by the spread of the Omicron virus strain, real GDP fell by 1% quarter-on-quarter and year-on-year. Therefore, the GDP level in January-March compared to 2019 is +3.7% in the US, +0.6% in the EU, and -2.7% in Japan. By sector of demand, we can see a weak recovery in domestic private sector demand (personal consumption and corporate fixed investment). Under such circumstances, the most important task of monetary policy is to maintain an accommodative financial environment and firmly support the full recovery of domestic private sector demand.

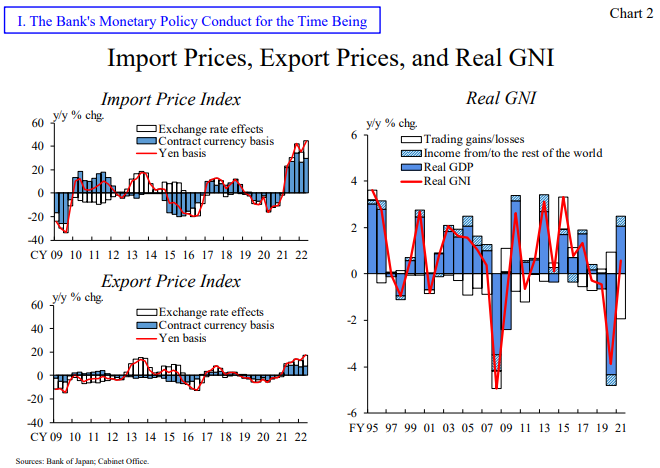

Second, as Japan is a commodity importer, income outflows triggered by the recent rise in international commodity prices have put its economy under downward pressure (Figure 2). On the one hand, the United States has been affected by the shale revolution, and many resources are produced domestically. The rise in commodity prices does not necessarily directly lead to the outflow of income. There is a measure of income that takes this change in terms of trade into account, called “real GNI”. This indicator is calculated by aggregating net receipts such as real GDP, overseas investment income, and trade revenue increases or decreases due to changes in the terms of trade caused by commodity price fluctuations. While Japan’s real GDP growth in fiscal 2021 was 2.1%, reflecting increased spending driven by the reopening of economic activity,But real GNI rose just 0.6% as higher commodity prices worsened the terms of trade.Also, the main reason for the deterioration in Japan’s terms of trade is not the weakening of the yen, but the rise in commodity prices in dollar terms. Rising dollar-denominated commodity prices will lead to higher import prices, but a weaker yen will simultaneously push up yen-denominated import and export prices, so the impact on the terms of trade is generally neutral. In any case, maintaining monetary easing is necessary to mitigate these adverse effects.

图2:Import Prices, Export Prices, and Real GNI

图2:Import Prices, Export Prices, and Real GNIThird, the 2% “price stability target” requiresstable and sustainableway to achieve. Consumer prices excluding food were little changed from forecasts in April, rising 2.1% year-over-year, ostensibly on track to reach the 2% target (Figure 3). The impact of last year’s cut in mobile phone bills has dissipated, and the main reason for the current price hike is the sharp rise in energy prices. on the one hand,Excluding food and energy, consumer prices rose 0.8%, which did not clearly reflect the rise in prices of all commodities other than energy.Consumer prices excluding food will rise 1.9% in fiscal 2022, according to the BOJ’s outlook, but the gains will narrow to 1.1% in 2023, when the boost from energy prices is expected to fade.Consumer price growth of 2% temporarily affected by higher energy prices does not mean that the 2% “price stability target” has been achieved, it is only true when it averages 2% after accounting for fluctuations in the economy and other factors Goals. To achieve this, it is necessary to maintain the current strong monetary easing policy to create a virtuous cycle of corporate earnings, employment and wage growth, and a modest rise in underlying inflation.I’ll explain in more detail the importance of wage growth in achieving the 2% goal later in this article.

图3:Consumer Prices in Japan, the United States, and the Euro Area

Monetary easing under yield curve control

For the above three reasons, the Bank of Japan has been actively promoting a strong monetary easing policy. As a specific measure, under the framework of yield curve control, in addition to short-term interest rates, the Bank of Japan also clarified the operational targets for long-term interest rates. At the April Decision-Making Meeting (MPM), we maintained our regular financial market regulation policy, with the short-term policy rate at -0.1% and the 10-year Treasury bond rate at “around 0%”. In addition, in the “assessment” in March last year, from the perspective of maintaining market functions to a certain extent and controlling the level of interest rates without compromising the effect of monetary easing, it was clarified that the fluctuation range of long-term interest rates should be kept at ±0.25%.Under this policy, the BOJ is currently buying long-term government bonds in the amount needed to keep the 10-year government bond rate in the range of 0% to ±0.25%.

In addition, at the decision-making meeting in April, the central bank also decided to conduct “fixed-rate purchase operations” at the yield of 0.25% of the 10-year Japanese government bond rate. Set a ceiling on interest rate volatility and clarify the central bank’s monetary easing stance. This is because announcing in advance that banks will conduct fixed-rate operations basically every working day will ensure market stability, as some in the market have been trying to infer the future policy stance of banks from whether they will conduct fixed-rate operations.

In fact, since the beginning of this year, even though long-term interest rates in Europe and the United States have continued to rise, long-term interest rates in Japan have remained in line with the adjustment policy and have not exceeded the 0.25% ceiling (Figure 4). Since the BOJ’s yield curve control operates to target long-term interest rates, the amount of government bond purchases is endogenous. The Bank of Japan has recently increased fixed-rate operations and government bond purchases, but the total amount of government bond purchases has not increased significantly compared to the past. Also, since the daily fixed rate operation began in May, bid volumes have been zero. We believe that, in addition to the “stock effect” of the purchase of government bonds (JGB) in the past, when the long-term interest rate exceeds 0.25%, the “announcement effect” of the Bank of Japan’s unlimited purchase of government bonds through fixed-rate operations is expected to market participants. formation had a significant impact.Regardless, long-term interest rates have held steady at low levels under yield curve control, keeping funding conditions such as commercial paper (CP), corporate bonds and bank loans loose and firmly supporting economic activity in Japan.

图4:Long-Term Government Bond Yields and the Bank‘s JGB Holdings

3. Strive for a stable and sustainable realization of the “price stability target” of 2%

Next I discuss a specific path to achieving the 2% “price stability target” in a stable and sustainable manner. In this regard, discussions at the BOJ’s workshop entitled “Price Development Issues Surrounding the Covid-19” held at the end of March were instructive. At the seminar, the staff of the Bank of Japan analyzed the differences in price changes highlighted in Europe, the United States and Japan under the epidemic, and had a heated discussion on why only Japan continued to experience low inflation, and mainstream Japanese economists also participated in the discussion. According to the discussion,We believe that achieving the 2% target in a stable and sustainable manner in Japan will be key to significant wage growth and a move away from years of zero service price inflation.We elaborate on this below.

Price volatility in the midst of Covid-19: Differences between Japan and Europe and the US

Let’s start by looking at inflation dynamics in Japan, the US and Europe amid the Covid-19 pandemic (Figure 3 above). U.S. consumer prices have been rising rapidly, currently at around 8 percent, or around 6 percent even after excluding energy. In terms of monetary policy response, the Fed until last summer said it chose to tolerate because price increases were temporary and that monetary easing would remain committed to supporting the economy as long as there were no secondary spillovers on wages or inflation expectations. In fact, the main driver of inflation at the time was cost-push factors, such as the automotive industry, which were strongly affected by supply bottlenecks and energy prices. However, U.S. inflation has since accelerated considerably, contrary to initial expectations. There are two backgrounds. First, the labor force participation rate has not fully recovered due to the vigilance of the epidemic. Second, the forces of aggregate demand have driven prices to generally rise, not only due to supply factors, but also due to continued strong economic growth. Under this circumstance, the labor supply and demand relationship has recently tightened, and the ratio of recruits to job seekers has reached an unprecedented high of about 2 times. Workers have been raising wage demands to deal with rising inflation, which has led to further increases in the price of services, including rent. As a result, the Fed raised interest rates by 0.25% and 0.5% in March and May, respectively, in an effort to curb wage and price spirals, and is signaling the need for further rate hikes in the future.

We believe that this policy response by the Fed will essentially contribute to the stability of the entire global economy by stabilizing the U.S. economy and prices. However, in the international financial and capital markets, amid persistently high U.S. inflation and an accelerating pace of interest rate hikes, some risks have been pointed out, such as a sharp correction in the prices of risky assets such as stocks and capital outflows from emerging economies. It is necessary to pay close attention to the future trends of these risks.

current,EURThe growth rate of consumer prices in the region also increased significantly. Headline inflation is currently around 8%, and excluding energy it is also above 4%. With its close economic and geographical ties to Ukraine, energy prices have risen further, and the economic outlook has become increasingly uncertain, leaving the ECB in a dilemma between suppressing inflation or supporting the economy. The ECB has so far held off on raising interest rates focused on supporting the economy, but faced with the secondary spillover effect of recent price increases on wages and inflation expectations, Lagarde said it would raise rates in July-September.

In contrast, consumer prices in Japan, while rising, remain at around 2 percent, lower than in Western countries. But at the same time, it also highlights Japan’s long-standing difficulty in raising prices. In other words, commodity prices in Japan exhibit cyclical fluctuations in line with the supply-demand gap, similar to those in Europe and the United States, albeit to a different degree. On the other hand, unlike Europe and the United States, service prices in Japan have remained extremely rigid and have barely risen even during the pandemic.

In order for Japan’s annual inflation rate to reach around 2%, service prices need to maintain a contribution of around 2% to the CPI, while commodity prices need to fluctuate periodically around 2%. At this point, a comparison of the distribution of price changes in consumer price categories in Japan and the United States shows that the United States had some differences between categories in pre-pandemic increases, mostly in services, around 2% (Figure 5). ).In Japan, the price change rate for the vast majority of goods is zero, and that hasn’t changed significantly since the outbreak.

图5:Price Change Distributions in Japan and the United States

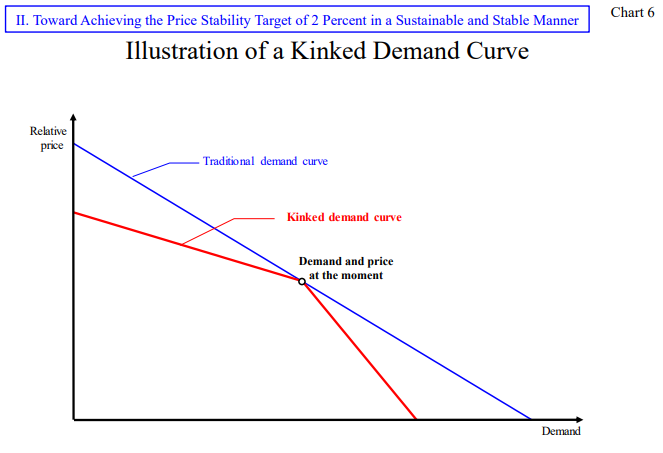

The biggest reason the Bank of Japan has failed to achieve its 2% target despite massive monetary easing over the past nine years is that the “zero inflation norm” has been extremely persistent. In the United States, the 2% norm is not commonly followed by all economic entities, entities that follow the 1% and 3% exist, and the 2% is just an average. On the other hand, Japan’s zero inflation norm means everyone is doing the same, “without changing the price tag.” Economists point to the existence of an inflection demand curve as one of the backgrounds for the immovability of prices in Japan (Figure 6). In other words, the demand curve faced by individual companies, even if the price rises slightly, the demand will fall sharply, and the demand will not increase significantly when the price drops slightly, so “no price tag change” has become the optimal pricing for Japanese companies Behavior.

图6:Illustration of a Kinked Demand Curve

图6:Illustration of a Kinked Demand CurveThe importance of rising wages

The key to changing this is to raise wages. This means increasing labor costs faced by all businesses, creating a situation where prices, including service prices, are increasing year by year, and increasing consumer tolerance for price increases by raising wage income. (This statement was questioned in the Diet on June 8, and Kuroda immediately withdrew the statement that “households’ tolerance for price increases is increasing”) To do this, it must first be through sustained and powerful monetary easing. To maintain the tight labor supply and demand situation, and secondly to ensure that the wage growth rate determined in the annual labor-management negotiations can reflect the actual increase in inflation.

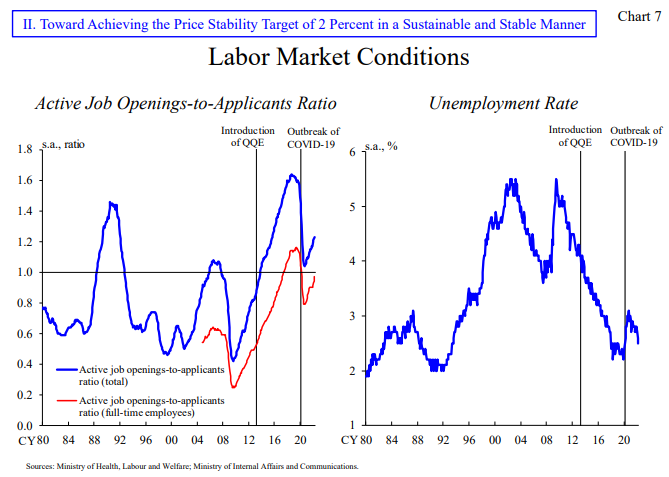

First, let’s look at the tightening of labor supply and demand. Since 2013, economic activity has been pushed up by the central bank’s strong monetary easing policy, and labor supply and demand have continued to tighten. By around 2018, before the spread of the epidemic, the effective job vacancy rate had risen to 1.6 times, surpassing the peak during the bubble period, while the unemployment rate had fallen to a low level in the 2%-2.5% range (Figure 7). Against this backdrop, upward pressure on wages in the “external labor market” (where firms adjust for surplus and shortage of marginal labor) increased, and part-time hourly wages, which are sensitive to labor supply and demand, rose by around 3 percent. This tightening of labor supply and demand is expected to spill over into the “internal labor market,” which is centered on long-term employees within companies. This is because in Japan’s internal labor market, long-term employment practices for regular employees are largely maintained, and even in boom times, slack is often maintained at the expense of recession-time job security, and the rate of wage growth is often limited. . However, the slowdown in overseas economies has become evident since late 2018, and the direct impact of the COVID-19 pandemic in 2020, which has moderated labor supply and demand, has not led to an overall increase in wages for full-time employees. Looking ahead, as set out in the April 2022 Economic Activity and Price Outlook (the Outlook report), economic growth is expected to exceed potential growth for three consecutive years, beginning in fiscal 2022. In this case, the key is whether labor market conditions will tighten not only in the external labor market but also in the internal labor market, and whether this will lead to an overall increase in wages.

Next, let’s talk about the realization of wage growth that reflects real inflation. During times of deflation, including the economic recovery of the mid-2000s, many companies held off on increases in the wage base (base salary). In contrast, since 2013, the pace of price increases has increased modestly due to massive monetary easing, and wage base increases have recovered and have risen for nine consecutive years, including this fiscal year. However, average base growth over the past nine years has been around 0.5%, still low compared to Europe and the US, and even low compared to pre-deflationary Japan. One hypothesis presented at the workshop at the end of March was that households are unlikely to perceive, and be less likely to pay attention to, the increased cost of living due to price increases, given that price increases in recent years have been significantly lower than regular wage increases of around 2% on average price. This is also known in recent economics as “rational inattention”, where people tend to ignore information they judge to be unnecessary when making economic decisions. In any event, the validity of this hypothesis requires further theoretical and empirical testing, but the key point going forward is to what extent the recent 2% price increase will be factored into wage growth in the coming year and beyond.

Figure 7: Labor Market Conditions

Figure 7: Labor Market ConditionsSigns of a change in inflation expectations

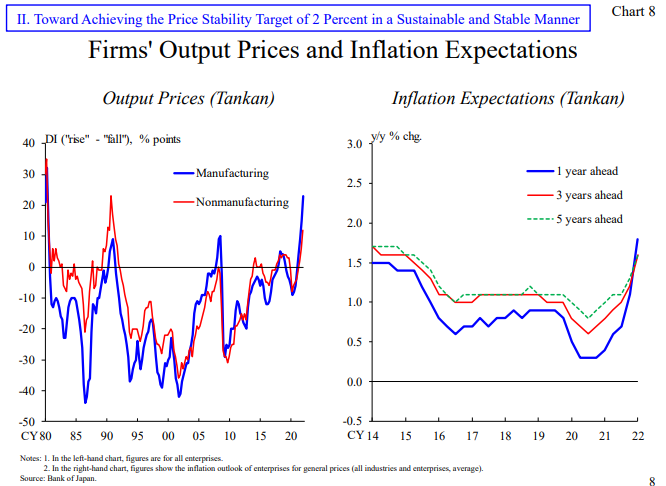

Both business and household inflation expectations and perceptions of inflation have changed recently. In terms of business perceptions of inflation, the March Tankan shows that the output price DI (diffusion index, considered to indicate the price-setting stance for the next three to six months) has risen since the early 1980s (i.e. the second The highest level in manufacturing since the second oil shock) and the highest level in non-manufacturing since the beginning of 1990, when the bubble ended (Graph 8, left-hand panel). The Tankan also shows that business inflation expectations for general prices in the coming year have risen markedly to the highest level since the survey began, while expectations for the next three and five years have also risen to near-peak levels (right-hand side of Figure 8). panel).

图8:Firms‘ Output Prices and Inflation Expectations

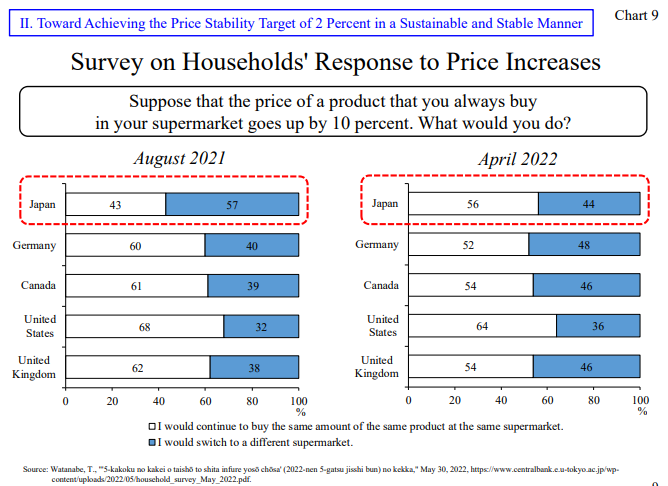

图8:Firms‘ Output Prices and Inflation ExpectationsAmid the more aggressive pricing stance by companies, Japanese households are also becoming more tolerant of price increases, which can be seen as an important change from the perspective of achieving sustainable price increases. In this regard, Professor Nobu Watanabe of the University of Tokyo conducted an interesting survey (Fig. 9). Specifically, he conducts regular surveys in five countries, including Japan, of households’ responses to the question “What would you do if the price of a product in a familiar store increased by 10 percent.” In the last survey last August, more than half of Japanese households said they would “move to another store” because of higher prices, exactly as suggested by the inflection point demand curve. The results stand in stark contrast to Western countries, where more than half of respondents said they would accept a price increase and continue to buy at the same store. In a survey conducted in April this year, Japan’s findings changed. In other words, the number of respondents who said they moved to another store decreased significantly, with more than half of respondents saying they would accept the price increase and continue to buy at the same store, which is consistent with the results in Europe and the US. While the results themselves are subject to large margins of error, there is a hypothesis that the “forced savings” accumulated under the COVID-19 movement restrictions may lead to a greater tolerance of households to higher prices. anyway,The key points now are how to maintain a favorable macroeconomic environment as much as possible while Japanese households accept price increases due to factors such as forced savings, and how to align this with real wage growth (including base growth) from fiscal 2023 onwards Get in touch.

图9:Survey on Households‘ Response to Price Increases

图9:Survey on Households‘ Response to Price Increases4 Conclusion

I talked today about why the Bank of Japan believes monetary easing is necessary and the importance of wage growth to sustainably and steadily achieve its 2% price stability target.

Japan’s economy is still recovering under the haze of the epidemic, and its income is also under downward pressure from rising commodity prices. It simply does not have the conditions to tighten monetary policy.Our priority is to firmly support economic activity by maintaining a strong monetary easing policy persistently on top of the current yield curve control. Unlike foreign central banks, the BOJ does not face trade-offs between economic stability and price stability, so it is well-positioned to continue stimulating aggregate demand from a monetary perspective.

In its April outlook report, the Bank of Japan also released its outlook for consumer prices (excluding food and energy) to clarify quantitatively its outlook for price benchmarks. According to this outlook, consumer price growth is expected to rise to around 1.5% year-on-year in fiscal 2024 against the backdrop of an improving macro supply-demand gap and rising inflation expectations. To achieve this outlook and move towards a more stable 2% target, it is necessary to create a virtuous circle where wages and prices can rise in tandem.

The Bank of Japan intends to maintain its steadfast monetary easing stance in order to provide a macroeconomic environment conducive to wage growth, and to link the recent increase in inflation expectations and changes in price increases tolerance to continued price increases.

Author: Haruhiko Kuroda, Source: BOJ; Translator: Xiong Yong, Source: Wisburg

Massive information, accurate interpretation, all in Sina Finance APP

Responsible editor: Guo Jian