Original title: The non-performing rate has declined for 6 consecutive years,Jiangyin BankLast year, revenue increased slightly, and net profit increased by more than 20%

Source: China Times Network

Reporter Fu Bixiao

On January 18, Jiangyin Bank (002807.SZ) released its 2021 performance report. As of the end of 2021, the non-performing loan ratio of Jiangsu Jiangyin Rural Commercial Bank was 1.32%, which has been declining for six consecutive years. The total assets of Jiangyin Bank exceeded 150 billion yuan, a year-on-year increase of 7%. The total amount of deposits and total loans also increased by more than 10 billion yuan compared with the beginning of last year.

In the whole of last year, Jiangyin Bank realized a net profit attributable to shareholders of listed companies of 1.277 billion yuan, an increase of more than 20% year-on-year. But the bank’s operating income growth was small, up just 0.5% from 2020

Decreased defective rate

Jiangyin Rural Commercial Bank, formerly known as Jiangyin City Credit Cooperative Union, is a local joint-stock commercial bank established on the basis of the original 35 legal person credit cooperatives and 3 urban credit cooperatives in Jiangyin City. It is one of the first three joint-stock rural commercial banks in the country. .

Last year, Jiangyin Bank’s operating income did not grow significantly, but its net profit grew rapidly.

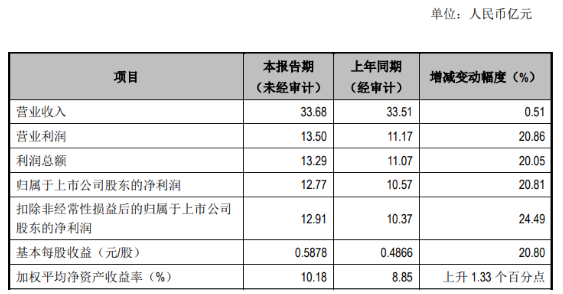

The performance report shows that in 2021, the operating income of Jiangyin Bank is 3.368 billion yuan, a year-on-year increase of 0.51%, and the net profit attributable to shareholders of listed companies is 1.277 billion yuan, a year-on-year increase of 20.81%.

(The table is from the 2021 performance report of Jiangyin Bank)

(The table is from the 2021 performance report of Jiangyin Bank)As of the end of 2021, the total assets of Jiangyin Bank were 153.099 billion yuan, an increase of 10.333 billion yuan or 7.24% over the beginning of the year; the total deposits were 114.459 billion yuan, an increase of 11.384 billion yuan over the beginning of the year; the total loans were 91.471 billion yuan, an increase over the beginning of the year 11.242 billion yuan.

(The table is from the 2021 performance report of Jiangyin Bank)

(The table is from the 2021 performance report of Jiangyin Bank)In terms of asset quality, as of the end of 2021, Jiangyin Bank’s non-performing loan ratio was 1.32%, down 0.47 percentage points from the beginning of the year. It is worth noting that Jiangyin Bank’s non-performing loan ratio has declined for six consecutive years. In addition, at the end of 2021, the provision coverage ratio of Jiangyin Bank was 331.04%, an increase of 106.77 percentage points from the beginning of the year.

In the investor relations event in September 2021, the relevant person in charge of Jiangyin Bank introduced that, on the one hand, Jiangyin Bank has established and improved the normalized recording and reflection mechanism for loans overdue for more than 60 days, continuously optimized the credit risk monitoring model, and made good progress in risk and hidden assets and assets. On the other hand, Jiangyin Bank accelerated the pace of retail transformation, reduced large-value loans, and continued to optimize and adjust its asset structure.

“China Times” reporter noticed that most of the small and medium-sized banks that recently announced their 2021 annual results have achieved a reduction in the non-performing ratio, such asBank of SuzhouThe non-performing rate decreased by 0.27 percentage points to 1.11%;Bank of NingboThe non-performing rate decreased by 0.02 percentage points to 0.77%;Changshu Bankdown 0.15 percentage points to 0.81%;Zhangjiagang BankThe non-performing ratio fell by 0.22 percentage points to 0.95%; the non-performing ratio of Chengde Bank fell by 0.08 percentage points to 1.72%.

“The general decline in the non-performing ratio reflects the improvement of the bank’s overall operating conditions and asset quality, which is related to the steady recovery of the overall macroeconomic environment, policy support, the bank’s own risk prevention and control, and the bank’s great efforts in risk disposal in recent years. It is expected from the domestic economy. Operating in a reasonable range, the bank’s overall non-performing provision is at a reasonable level, domestic banks are stable in operation, risks are controllable, and the overall non-performing loan will remain low.”Everbright BankAnalyst Zhou Maohua told a reporter from China Times.

However, Zhou Maohua also pointed out that due to the imbalance of regional economic and industrial development, as well as the differences in banks’ own risk control, the non-performing conditions of different banks are also different. At present, the global epidemic prevention and economic situation is still complicated, and the uneven domestic economic recovery has not fully returned to normal. Recently released data show that the operating conditions of banks are differentiated, and the scale of non-performing loans of some banks has increased significantly. Risk prevention and disposal cannot be relaxed.

Intermediate business growth

The growth of intermediary business income is a highlight of Jiangyin Bank’s operations.

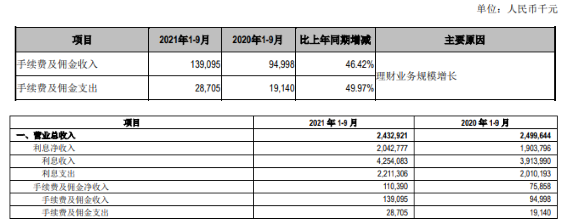

Previously, the third quarterly report for 2021 showed that the net fee and commission income of Jiangyin Bank in the first three quarters of last year was 110 million yuan, a year-on-year increase of 45%, and the fee and gold income and expenditure increased by nearly 50% year-on-year, mainly due to the scale of wealth management business. increase.

(The table is from the third quarterly report of Jiangyin Bank in 2021)

(The table is from the third quarterly report of Jiangyin Bank in 2021)However, according to the data disclosed in the third quarterly report, net interest income is still the main source of Jiangyin Bank’s income. The total operating income of Jiangyin Bank in the first three quarters of last year was 2.433 billion yuan, of which net interest income reached 2.043 billion yuan.

The relevant person in charge of Jiangyin Bank once revealed in an investor relations event in November 2021 that Jiangyin Bank has obtained the qualification for fund sales agency business, and said that in the future, Jiangyin Bank will “make full use of the bank’s many outlets and high online business recognition. advantages, further strengthen the use of scientific and technological means, increase theOnline and offlineMarketing efforts will continue to increase the proportion of intermediary business income.

In terms of expanding non-interest income, Jiangyin Bank launched the “Furong Wealth Management” brand, and at the same time developed intermediate businesses such as funds, insurance, and precious metals. And with the help of mobile banking, WeChat applet, WeChat banking and other tools, Jiangyin Bank has realized the comprehensive onlineization of intermediate business products.

In addition, Jiangyin Bank has also made certain achievements in serving small and micro enterprises.

In recent years, under the guidance of policies, the business of large and medium-sized banks has continued to sink, which has brought a certain impact to local rural commercial banks such as Jiangyin Bank, and the competition in the inclusive small and micro market has also become more intense.

In terms of inclusive business, Jiangyin Bank focuses on promoting the work of “whole village credit extension, whole town credit extension and whole city credit extension”. As of the end of September 2021, the bank has collected 244 administrative villages for review, and completed offline pre-sale of 215 administrative villages. credit. The balance of inclusive farmers and inclusive small and micro loans (excluding discounts) of Jiangyin Bank was 19.96 billion yuan, a net increase of 5.17 billion yuan compared with the beginning of the year, an increase of 35%.

Massive information, accurate interpretation, all in Sina Finance APP

Responsible editor: Li Linlin