According to the “Analysis of the National Passenger Car Market” issued by the Passenger Car Market Information Joint Conference, the Sohu Automobile Research Office compiled the national passenger car market in November 2021, as follows:

In November 2021, the national narrow passenger vehicle output was 2.229 million, a year-on-year decrease of 2.1%, of which the output of sedan was 1.046 million, a year-on-year increase of 0.1%; the output of SUV was 107.6, a year-on-year decrease of 2.1%; the output of MPV was 107,000, a year-on-year decrease of 19.7% %.

Retail sales: In November 2021, the national retail sales of passenger vehicles in the narrow sense was 1.816 million, a year-on-year decrease of 12.7%; among them, the retail sales of sedan vehicles was 892,000, a year-on-year decrease of 11.4%; the retail sales of SUVs was 841,000, a year-on-year decrease of 12.6%; MPV retail sales The sales volume was 84,000, a year-on-year decrease of 24.8%.

Wholesale sales: In November, the national wholesale sales of passenger vehicles in a narrow sense was 2.15 million, a year-on-year decrease of 5.1%. Among them, the wholesale sales of cars were 1.015 million, a year-on-year decrease of 3.5%; the wholesale sales of SUVs were 1.026 million, a year-on-year decrease of 5.5%; and the wholesale sales of MPVs were 110 thousand, a year-on-year decrease of 14.7%.

(3) Monthly sales trend chart of domestic passenger vehicles in a narrow sense from 2017 to November 2021

(4) New energy market (production, retail/wholesale sales)

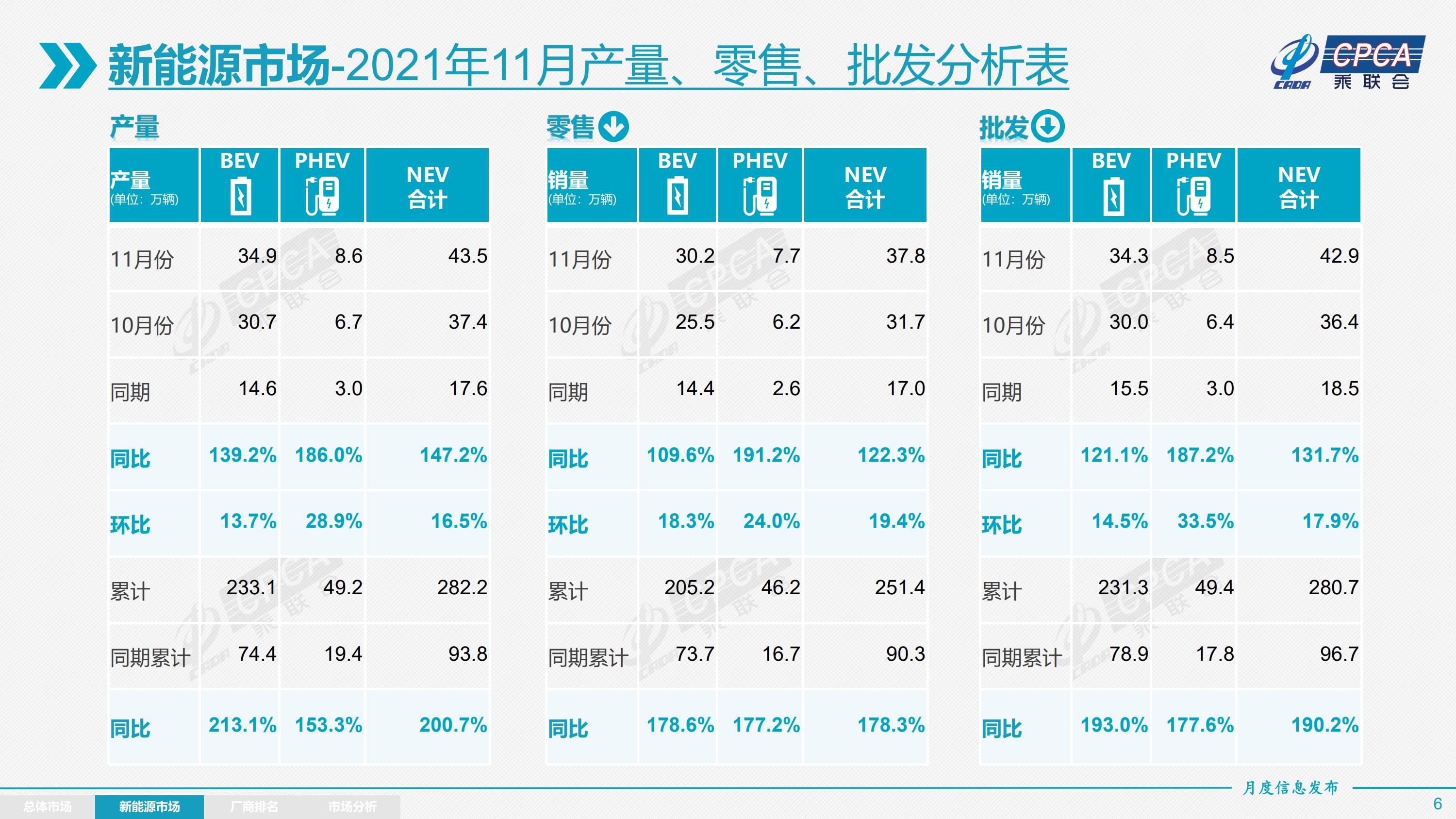

In November, the output of new energy passenger vehicles reached 435,000, a year-on-year increase of 147.2%; among them, the output of BEV was 349,000, a year-on-year increase of 139.2%; the output of PHEV was 86,000, a year-on-year increase of 186.0%.

In November, retail sales of new energy passenger vehicles reached 378,000 units, a year-on-year increase of 122.3%; among them, retail sales of BEV were 302,000 units, a year-on-year increase of 109.6%; retail sales of PHEVs were 77,000 units, a year-on-year increase of 191.2%.

In November, the wholesale sales of new energy passenger vehicles was 429,000, a year-on-year increase of 131.7%; among them, the wholesale sales of BEV was 343,000, a year-on-year increase of 121.1%; the wholesale sales of PHEV was 85,000, a year-on-year increase of 187.2%.

(5) Sales trend of new energy market from 2017 to 2021 November

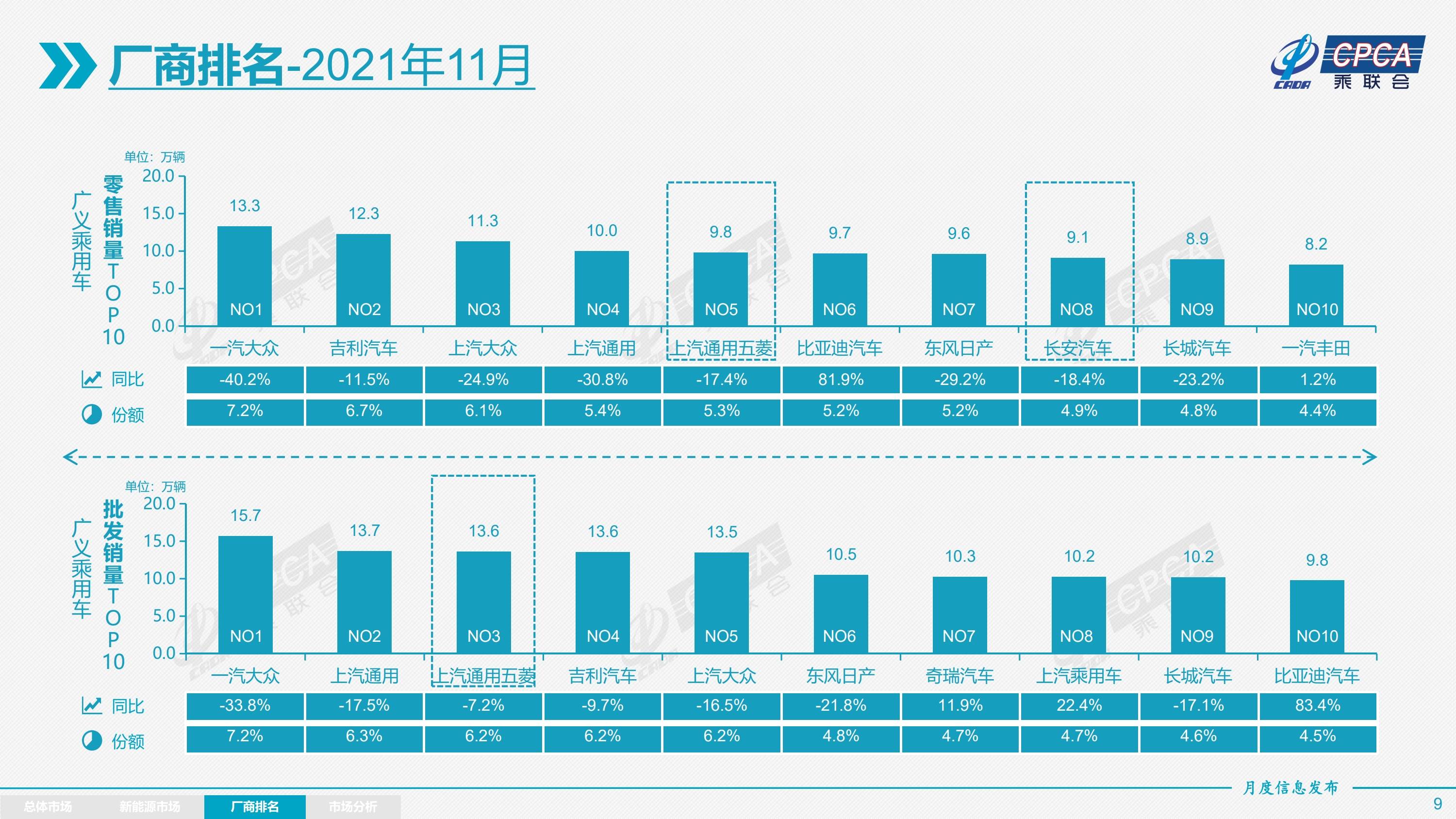

(6) Ranking of passenger car manufacturers in a narrow sense (retail sales and wholesale sales in November)

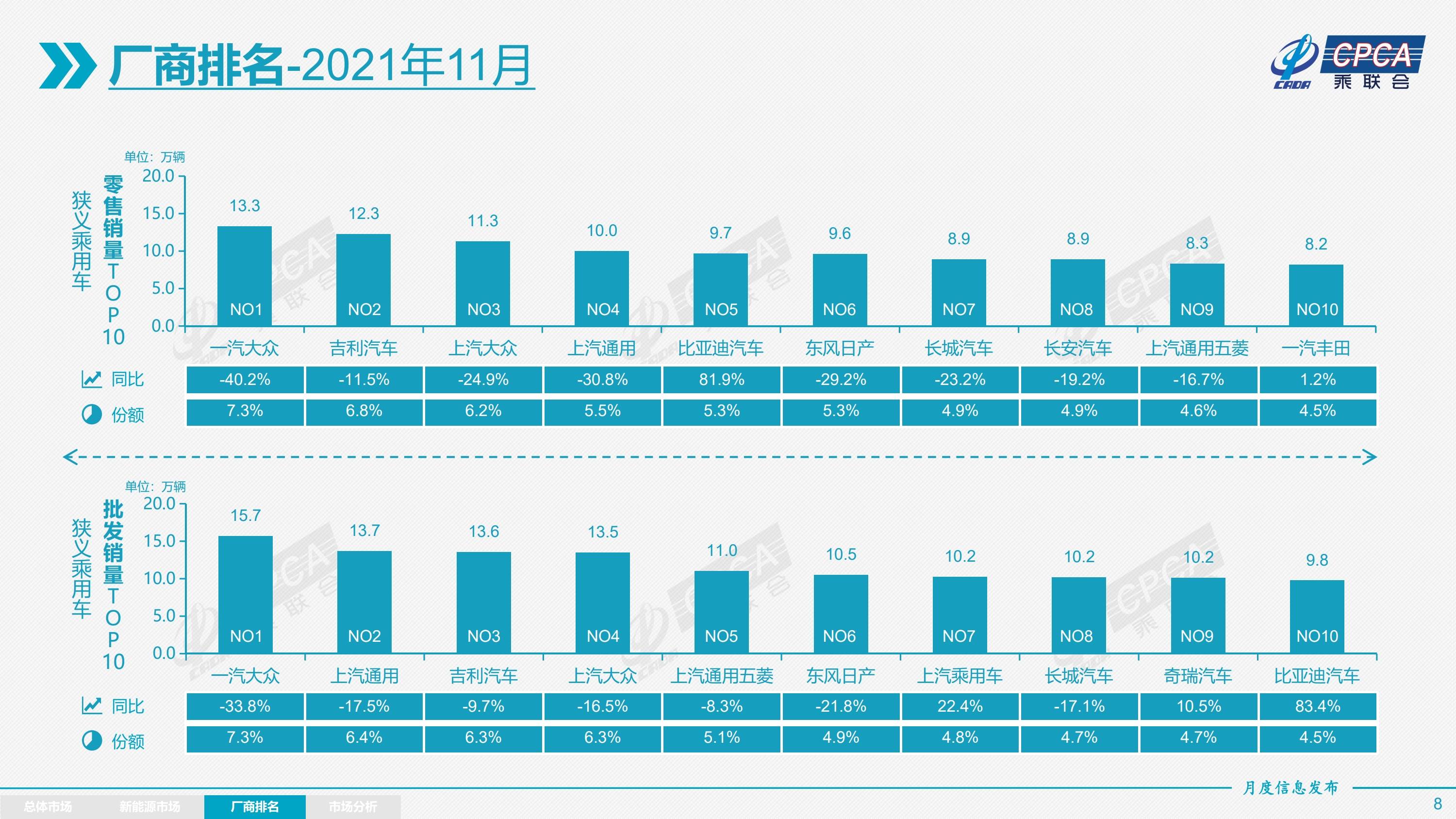

Narrowly defined passenger vehicle retail sales: In November, FAW-Volkswagen remained firmly at the top of the list, with sales of 133,000 vehicles, a year-on-year decrease of 40.2%, and a market share of 7.3%; Geely Automobile ranked second with sales of 123,000 vehicles, a year-on-year decrease of 11.5%. The market share is 6.8%; SAIC Volkswagen ranks third, with sales of 113,000 vehicles, a year-on-year decrease of 24.9% and a market share of 6.2%.

Narrowly defined passenger vehicle wholesale sales: The top three in November were FAW-Volkswagen, SAIC-GM, and Geely Automobile, with wholesale sales of 157,000, 137,000, and 136,000, respectively.

(7) Ranking of passenger car manufacturers in a broad sense (retail sales and wholesale sales in November)

Generalized passenger vehicle retail sales: The top three in November were FAW-Volkswagen, Geely Automobile and SAIC Volkswagen.

Generalized passenger car wholesale sales: The top three in November were FAW-Volkswagen, SAIC-GM, and SAIC-GM-Wuling.

2. Review of the National Passenger Car Market in November

retail: In November 2021, the retail sales of the passenger car market reached 1.816 million units, a year-on-year decrease of 12.7%, and a decrease of 6% compared to November 2019. The overall retail sales in November was not strong.

Retail sales in November increased by 6.0% month-on-month, compared to the 4% month-on-month growth in November in recent years. The retail trend in November this year has slightly improved.

The improvement of the auto market in November has a good environmental foundation. Due to good epidemic prevention measures, the epidemic situation was stable from the end of September to mid-November. The unblocking is conducive to the recovery of consumption in the auto market. The chip supply gradually improved at the end of September, which promoted a rise in production and sales in November.

The main unfavorable factor in November was the epidemic. The first was the spread and recurrence of the epidemic. On the one hand, it had a greater impact on the number of shop visits. On the other hand, it also hindered the repair of the service industry; secondly, it was the influence of supply and the pressure of falling economic indicators. In addition, employment expectations and confidence are weak, and consumer demand growth is sluggish, which is unfavorable for low-end and medium-end models. At present, the insufficient supply of chips and structural imbalance constraints have not been completely eliminated. The resources for best-selling models are still tight, and the constraints on the terminals still need time to adjust.

Due to the low inventory level of models on sale at the dealer level, although the inventory has rebounded, it has not reached the warning line. In November, terminal dealers continued to reclaim terminal preferential prices or increase the prices of derivatives. As the peak season is approaching, dealers have more motivation to pick up cars and stock popular models, which affects terminal sales.

The cumulative retail sales from January to November this year reached 18.041 million, a year-on-year increase of 6.1%, a drop of 2 percentage points from the growth rate from January to October. The reason for the dilution of the growth rate is mainly the impact of the high retail base from July to November 2020. From January to November this year, a year-on-year increase of 1.1 million new energy vehicles increased by 1.61 million, accounting for 146% of the total increase, and contributed 9 percentage points to the year-on-year growth rate from January to November.

In November, the retail sales of luxury cars were 210,000, a year-on-year decrease of 19%, a month-on-month increase of 17%, and a 4% increase from November 2019. Luxury cars continue to maintain structural stability, high-end trade-in demand that reflects consumption upgrades is still strong, and market competition has little impact.

In November, self-owned brand retail sales of 830,000 vehicles, an increase of 2% year-on-year, an increase of 8% month-on-month, and an 11% increase from November 2019. The domestic retail share of self-owned brands was 46.3%, an increase of 6.9 percentage points year-on-year. The wholesale market share was 46.9%, an increase of 6.2 percentage points over the same period. In addition, the industry chain of leading independent brand companies has strong resilience, effectively resolving the pressure of chip shortages, turning disadvantages into advantages, and gaining significant growth in the new energy market. Therefore, traditional car brands such as BYD and SAIC passenger cars have shown high growth year-on-year.

In November, mainstream joint venture brands sold 780,000 vehicles, down 23% year-on-year, up 1% month-on-month, and down 21% from November 2019. The retail share of Japanese brands in November was 22.2%, a decrease of 1 percentage point year-on-year. The retail share of the US market reached 9%, a year-on-year decrease of 0.6%. The share of legal systems increased by 0.3%, and the supply of German brands was gradually improving.

Export: In November, the Passenger Vehicle Association exported 170,000 vehicles (including complete vehicles and CKD), a year-on-year increase of 79%, and new energy vehicles accounted for 22% of the total exports. In November, the export of self-owned brands reached 130,000, a year-on-year increase of 26%, and the export of joint ventures and luxury brands was 39,000, a year-on-year increase of nearly 4 times.

Production: In November, 2.229 million passenger vehicles were produced, a year-on-year decrease of 2.1% and a month-on-month increase of 13.9%, showing a strong performance. Among them, luxury brand production increased by 3% year-on-year and 20% month-on-month; joint venture brand production decreased by 14% year-on-year and month-on-month growth by 17%; self-owned brand production increased by 10% year-on-year and month-on-month growth by 10%; cumulative production from January to November was 18.486 million vehicles. A year-on-year increase of 7.7%. The impact of the recent chip shortage has improved significantly. Luxury brands and joint venture brands have suffered large losses in the early stage, and the recent improvement has been significant.

wholesale: Manufacturer’s wholesale sales volume in November was 2.15 million vehicles, an increase of 8.9% month-on-month, a decrease of 5.1% year-on-year, and an increase of 6% from November 2019. The cumulative wholesale sales volume from January to November was 18.728 million, a year-on-year increase of 7.2% and a decrease of 212,000 from the same period in 2019. u Inventory: In the first three quarters of this year, inventory has been significantly depleted. In the past two months, manufacturers’ inventories have been replenished quickly. At the end of November, vendor inventory increased by 80,000 units from the previous month, and channel inventory increased by 190,000 units from the previous month; November of the past year was an important node for inventory building. In November of this year, the inventory was established well, laying the foundation for the year-end sales sprint.

In January-November 2021, manufacturers’ inventories will decrease by 230,000 vehicles, which is a larger reduction than that from January-November of previous years, forming a characteristic of strong destocking for four consecutive years. The channel inventory for January-November 2021 will be relatively reduced by 570,000 units. Compared with January-November 2020, the stock-out pressure of 200,000 units is still huge.

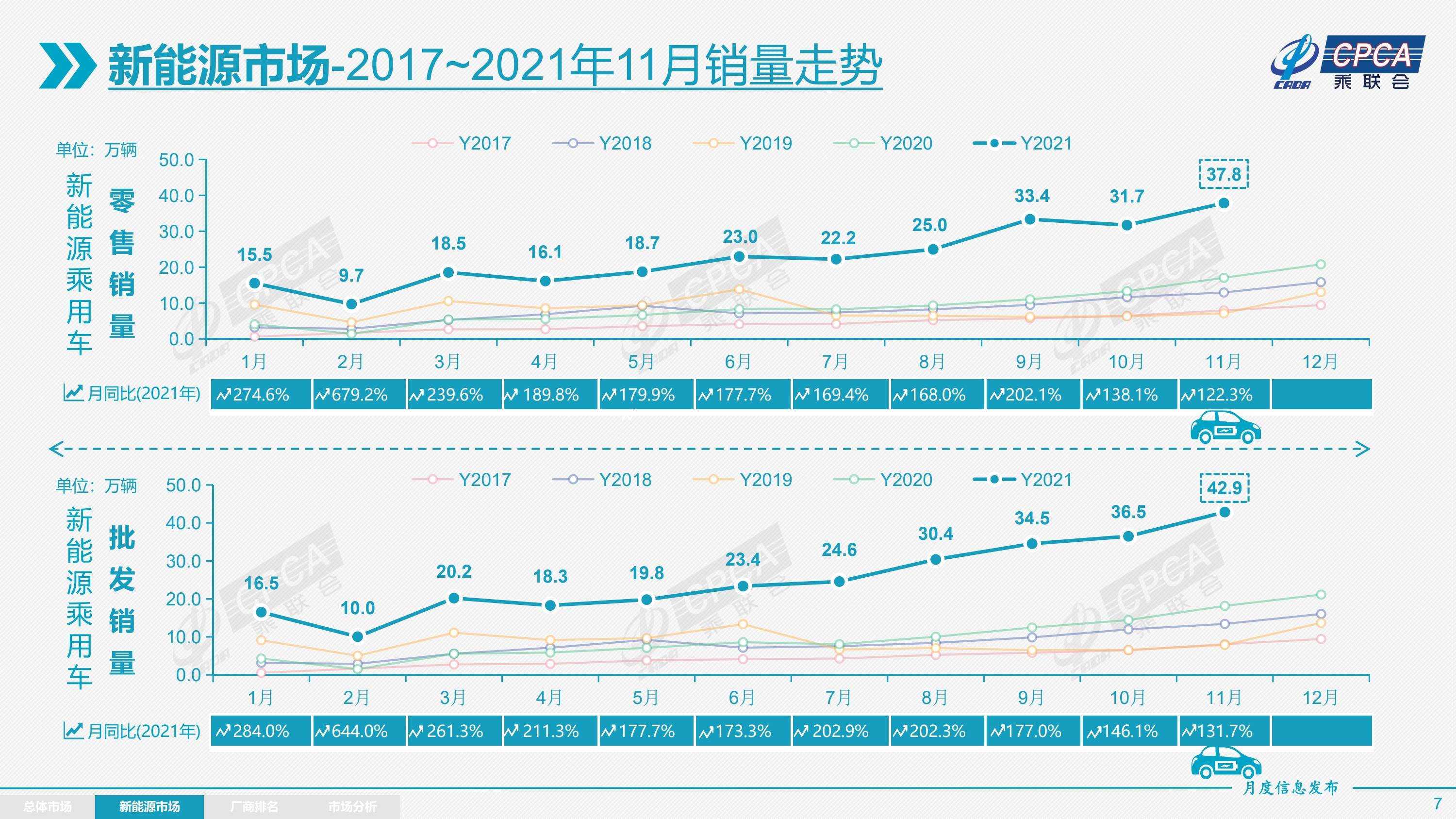

New energy source: In November, the wholesale sales of new energy passenger vehicles reached 429,000, an increase of 17.9% month-on-month and a year-on-year increase of 131.7%. From January to November, the wholesale of new energy passenger vehicles was 2.807 million, a year-on-year increase of 190.2%. In November, the retail sales of new energy passenger vehicles reached 378,000 units, a year-on-year increase of 122.3% and a month-on-month increase of 19.8%. From January to November, the retail sales of new energy vehicles amounted to 2.514 million units, a year-on-year increase of 178.3%. The trend of new energy vehicles and traditional fuel vehicles has formed a strongly differentiating feature, realizing the substitution effect on the fuel vehicle market, and spurring the auto market to accelerate the pace of transition to new energy.

1) Wholesale: In November, the wholesale penetration rate of new energy vehicle manufacturers was 19.9%, and the penetration rate from January to November was 15.0%, which is a significant increase from the 5.8% penetration rate in 2020. In November, the penetration rate of new energy vehicles among independent brands was 33.2%; the penetration rate of new energy vehicles among luxury cars was 24.6%; and the penetration rate of new energy vehicles among mainstream joint venture brands was only 3.9%. In November, the wholesale sales of pure electric vehicles were 343,000, an increase of 121.1% year-on-year; the sales of plug-in hybrid vehicles were 85,000, an increase of 187.2% year-on-year, accounting for 20%. In November, the sales of high-end electric vehicles grew strongly, and the low-end and mid-range sales trended strong. Among them, the wholesale sales volume of A00-class is 108,000, and the share is 31% of pure electric; the wholesale sales of A0-class is 53,000, and the share is 15% of pure electric; the A-class electric vehicles account for 25% of the pure-electric share, rebounding from the bottom; B-class electric The number of vehicles reached 91,000, an increase of 15% from the previous quarter, accounting for 26% of pure electric vehicles.

2) Retail: In November, the domestic retail penetration rate of new energy vehicles was 20.8%, and the penetration rate from January to November was 13.9%, a significant increase from the 5.8% penetration rate in 2020. In November, the penetration rate of new energy vehicles among independent brands was 37.4%; the penetration rate of new energy vehicles among luxury cars was 19.4%; and the penetration rate of new energy vehicles among mainstream joint venture brands was only 3.6%.

3) Exports: In November, the export of new energy vehicles maintained strong growth. Tesla China exported 21,127 units, SAIC Motor’s new energy exports of passenger cars 6,110, Geely Automobiles 470, Great Wall Motors 426, BYD 404, and other auto companies New energy vehicle exports are also gaining momentum.

4) Automakers: In November, the new energy passenger vehicle market was diversified. SAIC and GAC performed relatively well, while traditional automakers had outstanding highlights. BYD’s pure electric and plug-in hybrid two-wheel drive perform well. There are 14 companies whose manufacturer’s wholesale sales exceeded 10,000 units, which is a substantial increase from the previous period. Among them: BYD 90,546, Tesla China 52,859, SAIC-GM-Wuling 50,141, Great Wall Motor 16,136, Xiaopeng Motors 15,613, GAC Aian 15035 vehicles, 14482 Chery cars, 13,485 ideal cars, 13090 Geely cars, 12225 SAIC passenger cars, 11986 SAIC Volkswagen, 10878 NIO, 10705 FAW-Volkswagen, 10013 Hezhong.

5) New forces: In November, the sales of new forces such as Xiaopeng, Ideal, Weilai, Nezha, Zero Running, Weimar and other new power car companies performed better year-on-year and quarter-on-quarter, especially when Nezha exceeded 10,000 vehicles, zero running and Weimar The second-tier new forces in Zhejiang Province have also reached monthly sales of more than 5,000 vehicles. The mainstream joint venture brand North and South Volkswagen’s new energy vehicles wholesale 22,691 units, accounting for 62% of mainstream joint ventures. BBA’s luxury car company’s BMW new energy reached 5,194 vehicles, which is also very good. Other joint ventures and luxury brands are still waiting to be used.

6) General hybrid: In November, 66,400 ordinary hybrid passenger vehicles were wholesaled, a year-on-year increase of 44% and a month-on-month increase of 8%.

3. Outlook for the national passenger car market in December 2021

There are 23 working days in December, which is the same as that in December last year, and one more working day than November this year. This is conducive to the increase in production and sales. The wholesale recovery of enterprises is more obvious. It is expected that the shortage of resource supply in December will be further alleviated. The Spring Festival of 2022 On February 1, 11 days earlier than last year’s holiday, it is conducive to the accelerated recovery of the auto market in December, and the market can still look forward to it in December.

The economic situation at the end of the year and the beginning of the year is becoming increasingly complex and severe, but the node before the Spring Festival is a period of concentrated outbreak of first purchase users, and the performance of the auto market is bound to be stronger. At present, an important factor restraining the growth of the auto market is the downturn in the entry-level, which is also the combined effect of insufficient consumption power caused by changes in consumer confidence and disposable income. However, the previous backlog of orders has yet to be released, so car purchases before the Spring Festival also have a larger potential user group, and the market needs to create a better consumer environment. From the perspective of the regional market, in the face of the expiration of new license indicators in Guangzhou and other places, and the annual changes in new energy subsidy policies, retail sales in December are expected to be achieved.

As the epidemic has swept the world, many countries have encountered problems in automobile production, and the impact of the “core shortage” and the skyrocketing price of raw materials has been huge. The dark moment of automotive chip supply in the third quarter has passed. The improvement in chip supply was originally expected to bring production back to the level of November last year, but the actual growth rate was about 14% month-on-month, but it has not returned to last year’s level. The bottleneck factor of supply opacity is still .

The increase in production and sales in the auto market starting in October is the best time to increase inventory in the winter. The boom in the winter auto market must have inventory reserves in autumn. In November this year, the supply capacity of auto companies’ construction and storage inventory has not yet reached expectations, and the overall inventory is still at a low level. From the visits to the Guangzhou Auto Show, there is still a shortage of mid- and high-end models in some companies, and the inventory continues to be unable to make up. This has caused the difficulty of impulse at the end of the year, and part of the demand is expected to be transferred to 2022.

It is very important to rush production and sales under the epidemic. The more blooming epidemic is about to meet the Spring Festival and Winter Olympics. One is the largest population migration in the world, and the other is a large-scale sports event. In addition, the risk of importing Omicron mutant strains will continue to exist in the future, and the spread of new strains may be further enhanced, making it more difficult to prevent infection, which casts a shadow over the prevention and control of local epidemics this winter. . Therefore, it is very important for car companies to seize the time before the year to produce more and more transport, and to achieve effective inventory support for the terminal.

This year, the amount of precipitation in northern China is unusually high, and winter temperatures are also low. The sporadic spread of the epidemic has hindered public travel. Demand for new energy vehicles is strong, especially the enthusiasm of families to buy a second car. Both new powers and traditional car companies have set new highs recently. With the continuous advancement of capacity expansion, they have effectively catered to the needs of customers for new car experiences and promoted the market-oriented transformation of new energy demand.

4. High-energy-density batteries should be encouraged, and cobalt resource reserves for vehicles should be increased

The Ministry of Industry and Information Technology clearly stated: New energy vehicle power batteries are faced with the pressure of guaranteeing lithium, cobalt and nickel and other ore resources and rising prices, and it is necessary to improve the guarantee of key resources such as lithium, cobalt and nickel.

At present, the restricting factor in the development of new energy vehicles is the guarantee of resources such as cobalt, so there is an idea of developing lithium iron phosphate. The development of new energy passenger vehicles in 2021 is mainly due to the huge increase in lithium iron phosphate batteries.

The recent trend of high energy density of new energy vehicles in Europe and the United States is obvious. In particular, the US electric pickup truck market is about to grow substantially, increasing the demand for high-end batteries. We must also accelerate the promotion of high-energy-density battery loading to realize the full use of cobalt resources, turn cobalt ore stocks into on-board cobalt stocks, and implement policy guidance to effectively allocate cobalt ore resources and improve the security of nickel, cobalt and lithium resources.

Due to the huge size of the pickup truck market in the United States and the future US heavy truck products will also use ternary batteries, there will be a huge demand for ternary batteries worldwide in the future. The United States is developing new energy vehicles, and the current demand highlight is pickup trucks. The R1T newly launched by the American pickup truck startup Rivian is equipped with a 135-degree battery and requires 48 kWh of energy to travel 160 kilometers. Rivian plans to launch a larger 180 kWh battery pack in 2022, which will provide a range of 640 kilometers. At present, there is not much space for the internal battery layout of the pickup truck, and the 2170 battery provides 135 kilowatts of power, and the high energy density battery similar to the 4680 battery is estimated to reach 180 kilowatts.

Although the price of cobalt ore is high, we are subsidizing high-tech and cobalt resources. For consumers, when buying ternary batteries, because the value of cobalt ore is actually value-added, the ternary batteries bought by consumers may be the most precious resource when they scrap their cars, and the value of recycled batteries is also higher. Consumers should also be willing to accept.

The top three domestic battery companies this year are CATL, BYD and LG batteries, with different lines. China’s current external resource environment is still very good. At present, Chile, Congo, Indonesia, etc. have maintained good relations, encouraging high-energy-density batteries, increasing on-board cobalt resource reserves, and obtaining better resource guarantees for energy transition.

5. The penetration rate of new energy vehicles should be treated differently

At present, the penetration rate of new energy passenger vehicles from January to November this year has reached a level of about 15%. Passenger cars do not rely on subsidies but on the continuous rise of market demand. However, the penetration rate of large and medium-sized passenger cars has continued to decline in recent years with the withdrawal of subsidies.

The penetration rate of new energy trucks has gradually declined in recent years, from 2.1% in 2017 to 1.35% in 2018, and has remained below 1% since 2019.

The penetration rate of new energy buses continued to decline, reaching 24% in 2017 and 24% in 2018. Subsequently, the new energy bus market continued to weaken as subsidies fell, and it has now fallen back to 18.6%.

Commercial vehicle segments such as trucks and buses are facing technical bottlenecks in usage scenarios as a whole, greater reliance on municipal rights of road policies and public market, relatively low user price sensitivity, and long payment periods. These issues may be maintained in the short term. Market structure of “dojo in snail shell”.

The penetration rate of new energy in the passenger car market continues to rise, reaching 2.1% in 2017, 4% in 2018, and currently rising to 15%.

The penetration rate of new energy passenger vehicles varies greatly at various levels. Currently, A00 and B levels are relatively high. Due to different usage scenarios, new energy vehicles perform relatively prominently in some scenarios, especially short-distance mobility vehicles and the second family car. Therefore, the penetration rate of some market segments will be relatively high, especially when the penetration rate of A00-class cars reaches the level of 99%.

The penetration rate of A-class cars in mainstream families was around 7% in November. Because they need to be used in all scenarios, long and short distances are required, and relatively speaking, the living conditions of ordinary families also have certain restrictions, so traditional fuel vehicles are still At present, the penetration rate of the main A-class car group has not increased very quickly. In the near future, the plug-in hybrid and hybrid products of BYD, Great Wall, Geely and other independent brands are worth looking forward to. In particular, BYD Qin has formed a sales momentum of pure electric and plug-in hybrid in this market segment, providing new research and thinking directions for the evolution of energy technology of A-class vehicles.

Some organizations believe that it is difficult to increase the penetration rate of new energy in the future. In fact, it is differentiated. That is to say, at present, there is huge room for improvement in A, B, and A0 levels, while A00 At present, the penetration rate of the second class is relatively high, mainly relying on the downward exploration and expansion to replace the non-traditional motor vehicle market such as electric three-wheels and electric bicycles.

Due to the double difference between seasonality and products, in fact, the development of penetration rate is not a smooth linear increase. Therefore, it is difficult to simply think that the penetration rate we currently achieve will inevitably continue to increase substantially in the future. We judge that the penetration rate of new energy passenger vehicles should exceed 20% next year.

6. It is a reasonable choice to withdraw shares of individual joint venture brands

The most important task of a joint venture is to make a profit. If the company continues to be unprofitable, its existence value is also worth thinking about. At present, the operating status of joint ventures has a tendency of differentiation. With the overall rise of major independent brand enterprises, coupled with the dual-point policy of new energy vehicles and traditional vehicles, joint venture car companies need to have a more comprehensive system competitiveness to adapt to the ever-increasing market competition in China.

In the past two years, traditional cars in the auto market have continued to shrink. The internal structure of traditional cars is under pressure and independent brands are on the rise, causing the main position of joint venture brands to shrink rapidly. As the competitiveness of self-owned brand SUV products has increased significantly, the market for mid-to-high-end and high-profit models of joint-venture brands has been severely impacted. Joint venture companies in B-segment SUVs are showing strong performance between Japanese and German companies. The decline in SUV sales will inevitably lead to huge loss of profits. In recent years, the localization and cost reduction measures of joint ventures have not been comprehensive enough, especially when the pace of change of the foreign joint venture is slow, and the operating efficiency of individual joint ventures has deteriorated significantly.

This year’s core shortage pressure also caused a sharp decline in the profit of the auto industry. The profit of the auto industry in the third quarter was 92.3 billion yuan, a year-on-year decrease of 48%, and the profit margin was only 4.9%. Some joint ventures have suffered serious profit losses due to rigid supply chains.

Due to the slow improvement of the product power of some joint ventures and the lagging in the introduction of new technologies, it is difficult for individual joint ventures to significantly increase their competitiveness in the Chinese market, and they are completely unsuitable for double-point squeeze, and the pressure of loss will continue. In addition to the pressure of the joint venture partners from the liberalization of the joint venture share ratio in 2022, it is also a reasonable choice for one of the individual joint ventures to withdraw. The increase in the Chinese market by foreign parties also proves that the Chinese market has a strong charm.Return to Sohu to see more

.