Source: Pioneer Futures Author: Pioneer Futures

Research report text

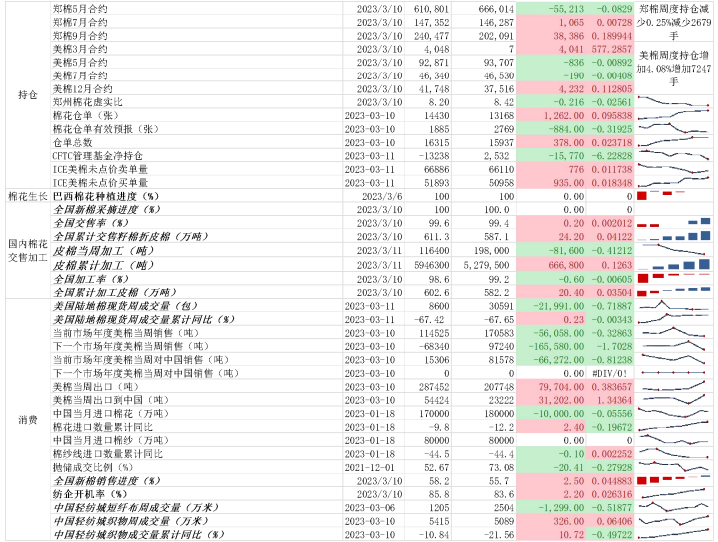

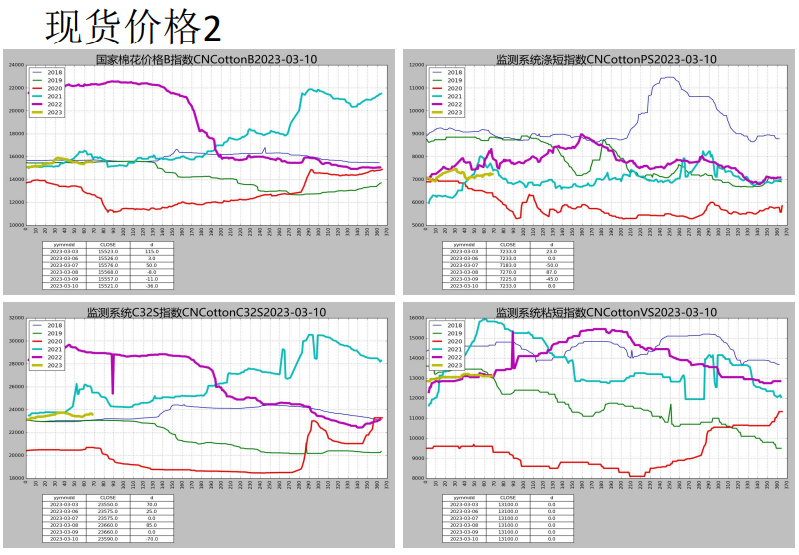

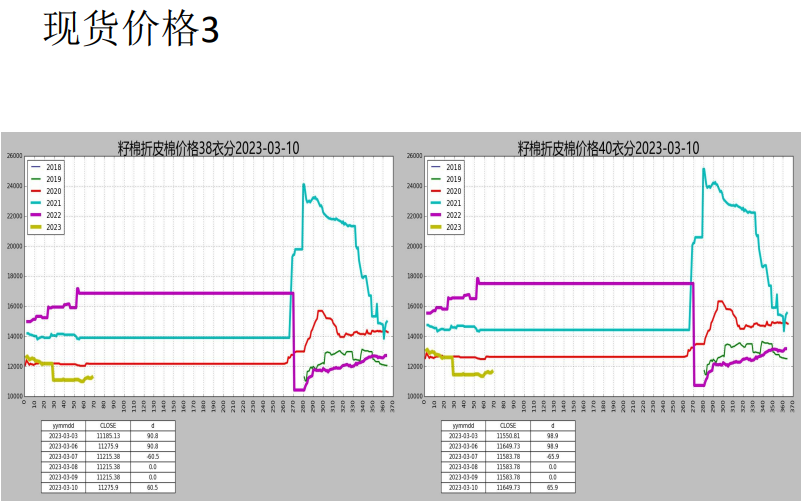

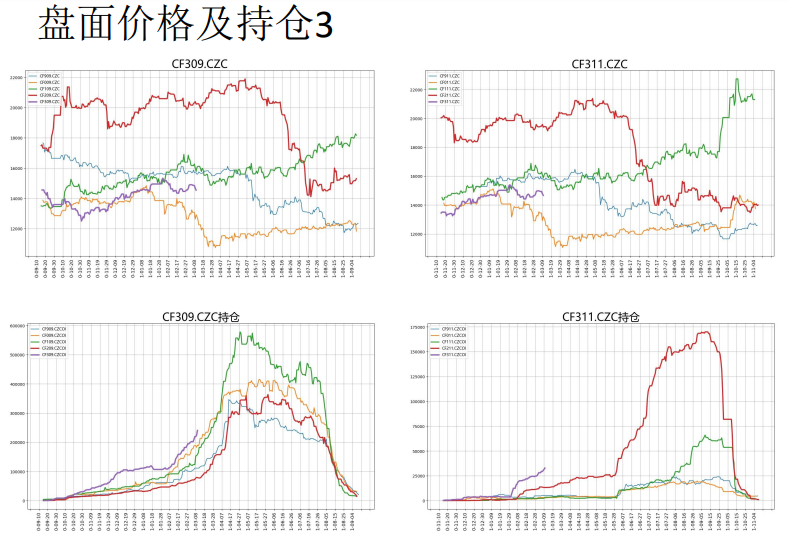

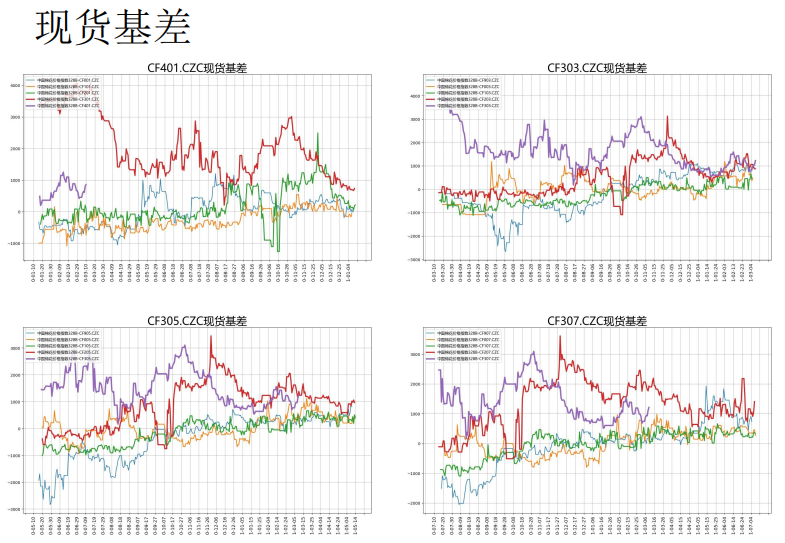

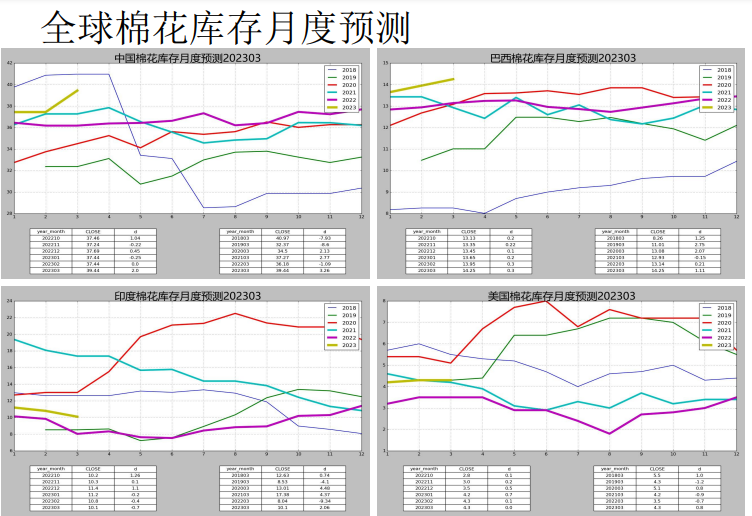

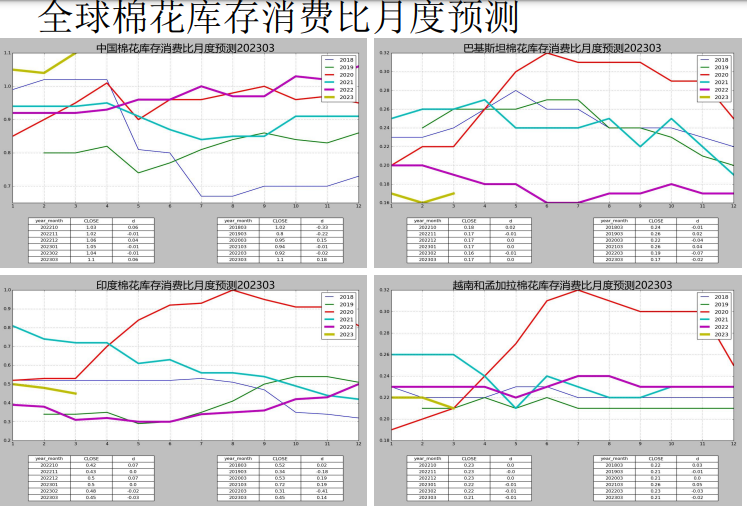

【Fundamental situation】

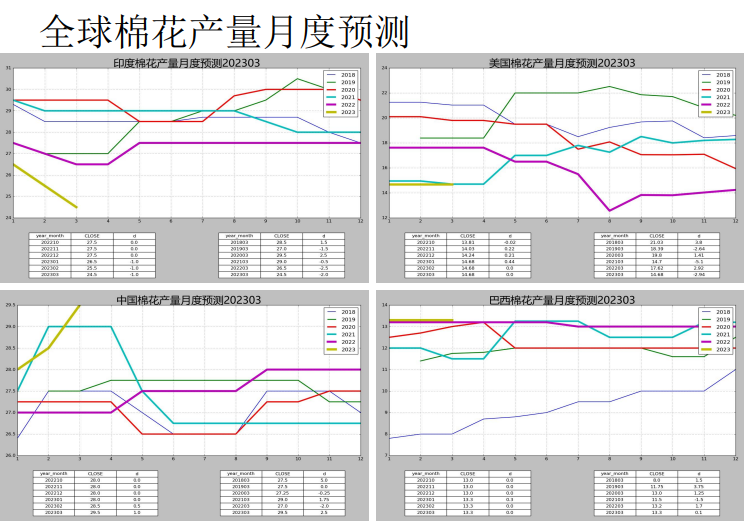

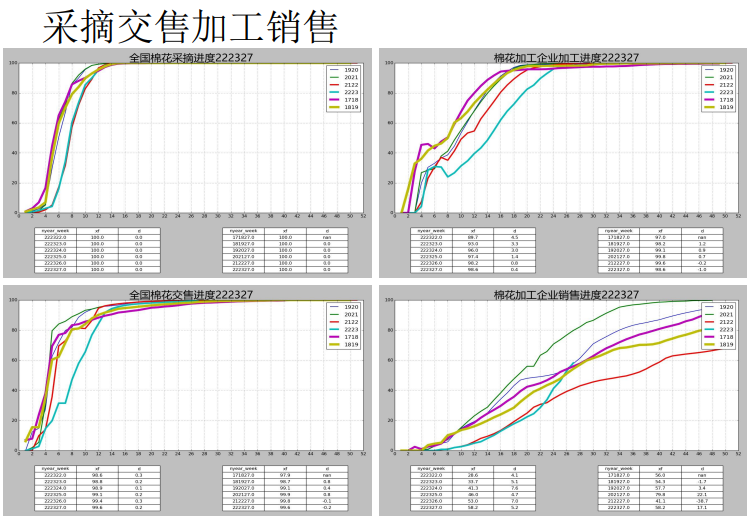

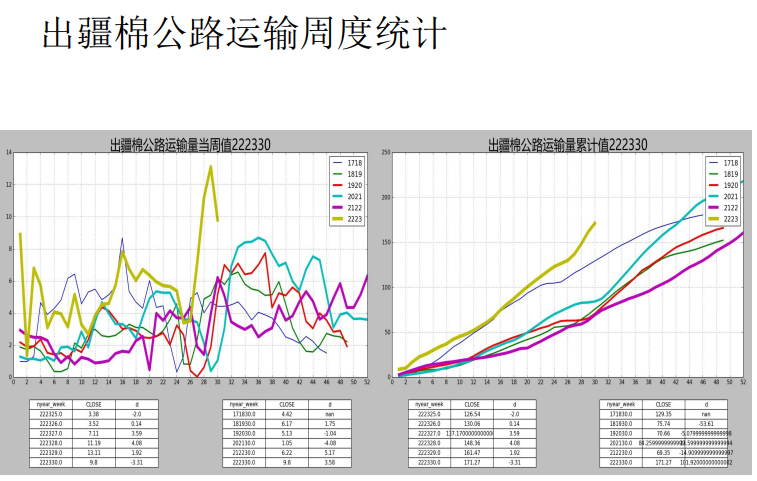

On the supply side, domestic new cotton processing is coming to an end. Brazilian cotton planting is drawing to a close. In the new season, the US cotton planting area is expected to decrease. The supply side has no drive for the time being.

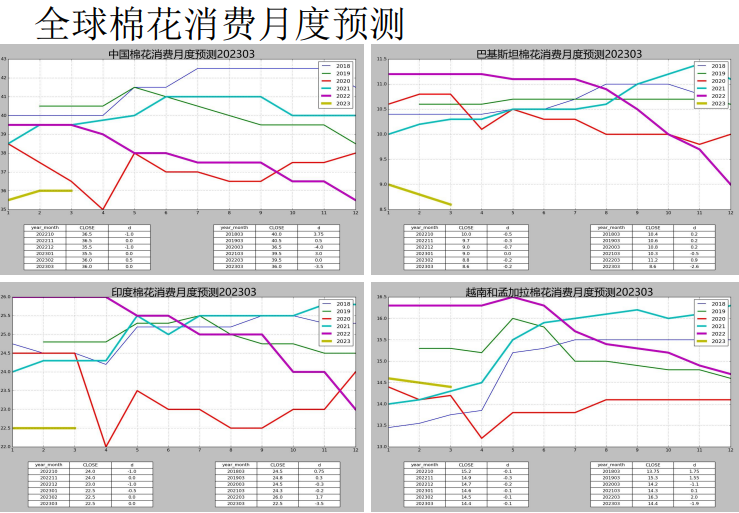

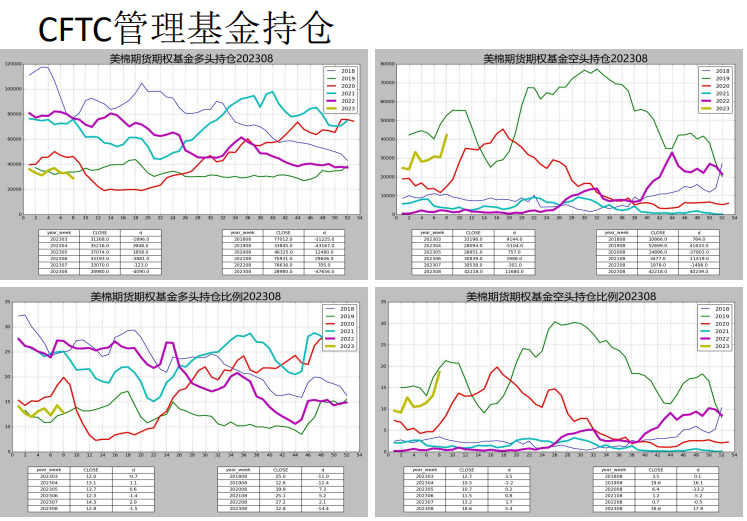

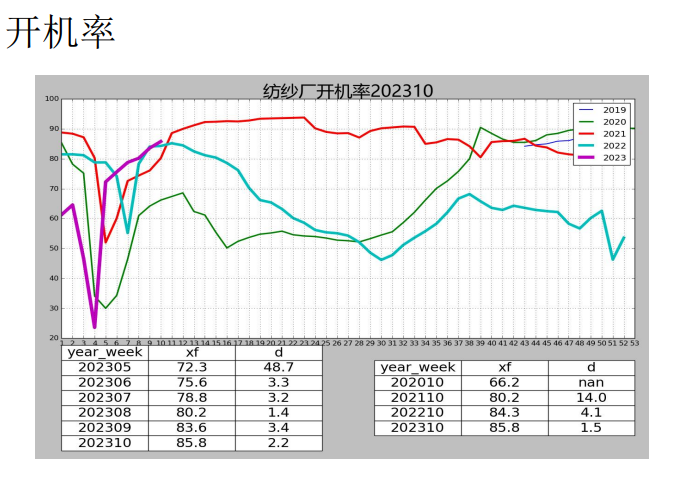

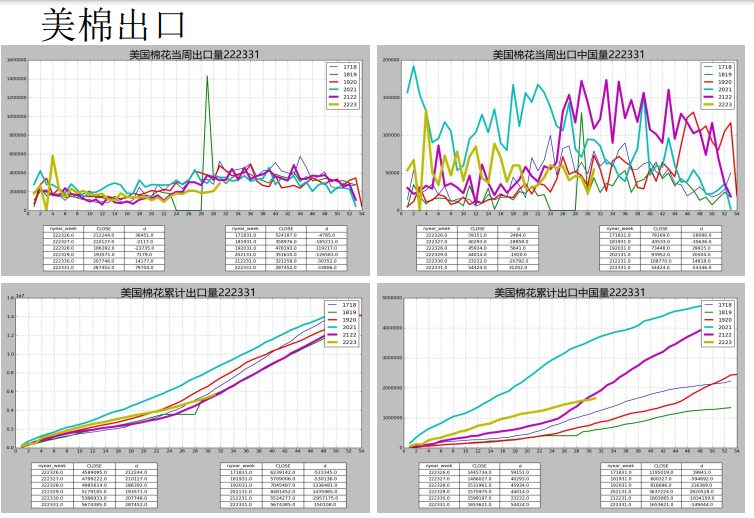

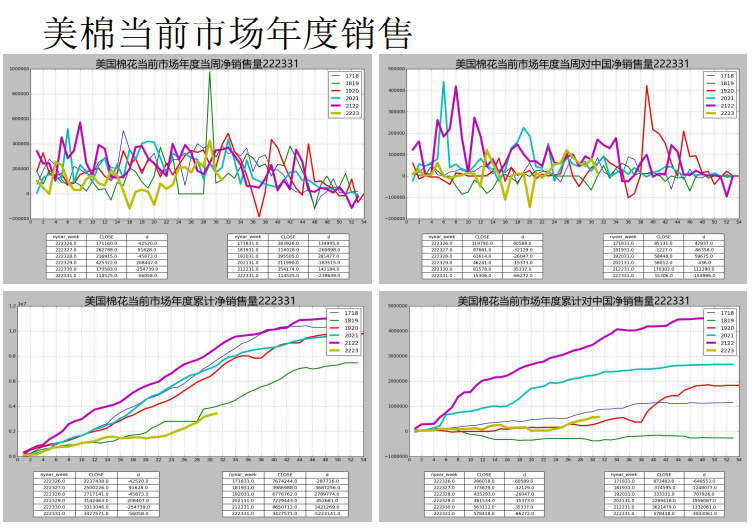

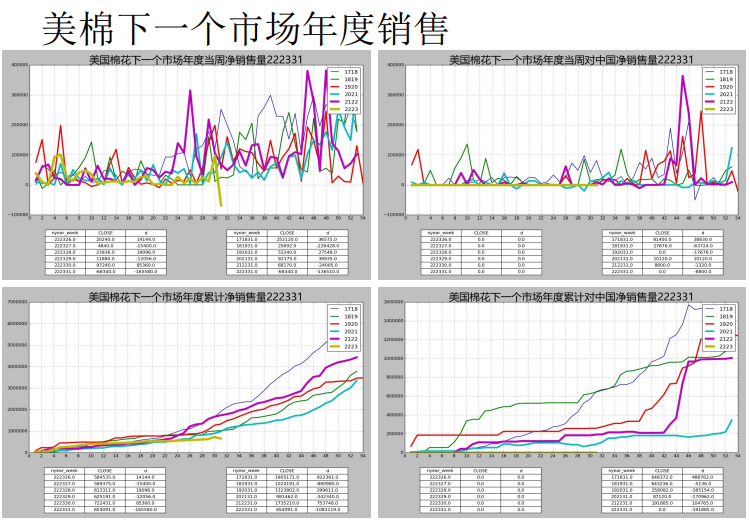

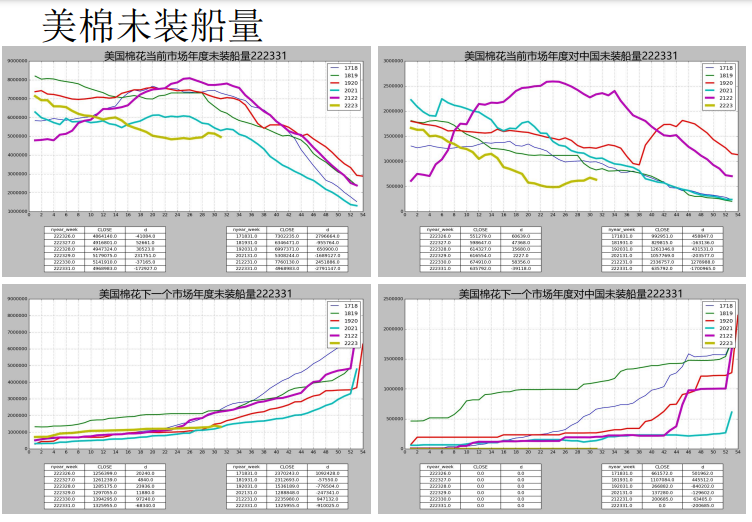

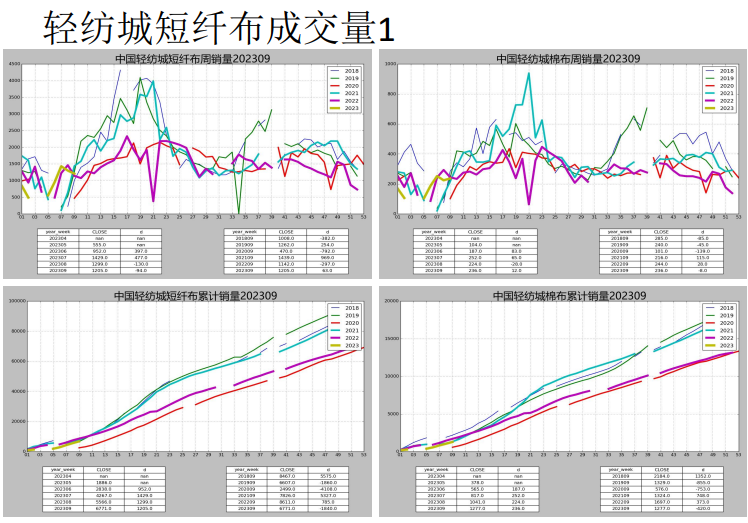

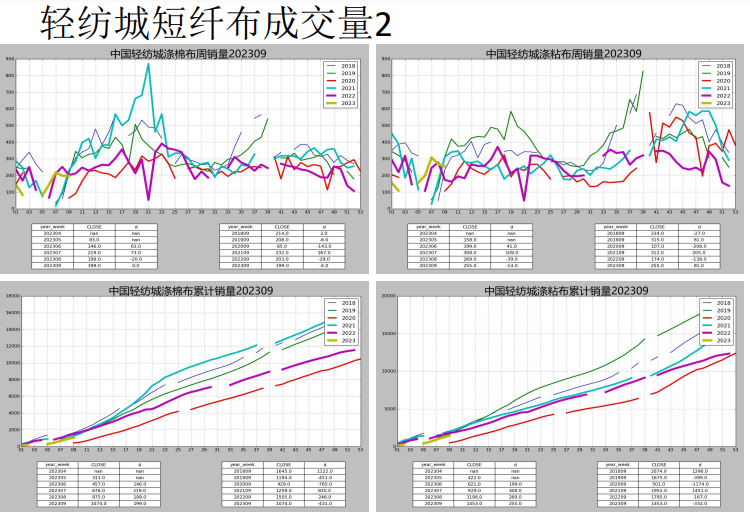

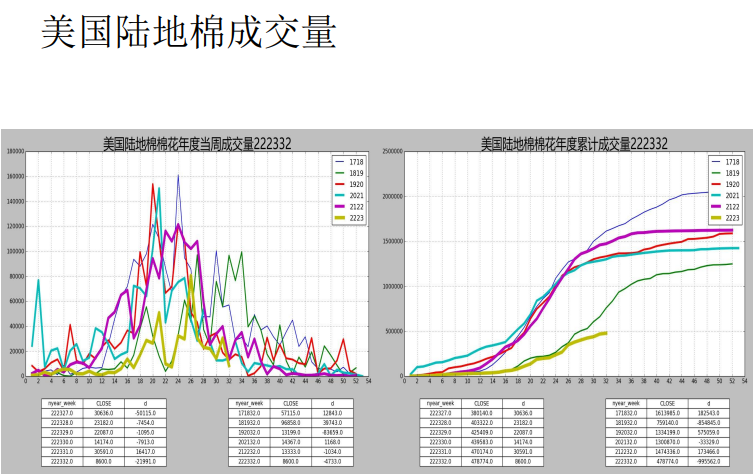

On the consumer side, US cotton export sales continued to decrease sharply week-on-week, sales to China decreased sharply, and shipments increased week-on-week. Domestic new cotton sales decreased slightly week-on-week. The operating rate of textile enterprises increased slightly week-on-week. The fabric transactions in China Textile City increased slightly week-on-week.

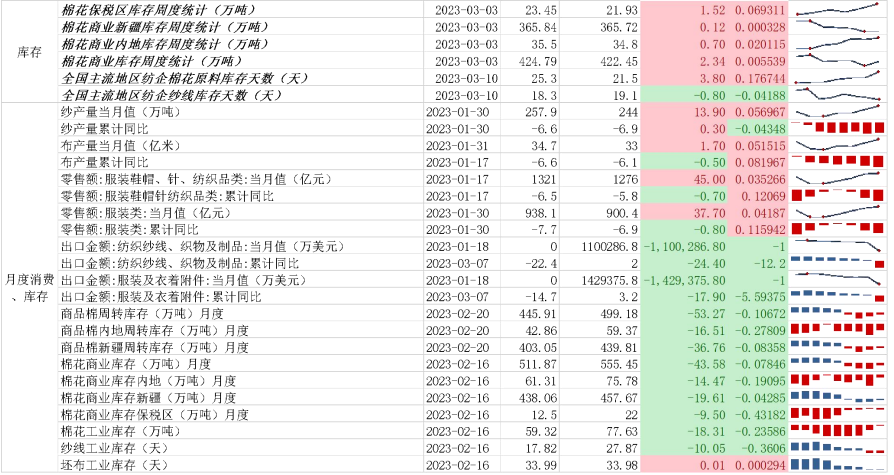

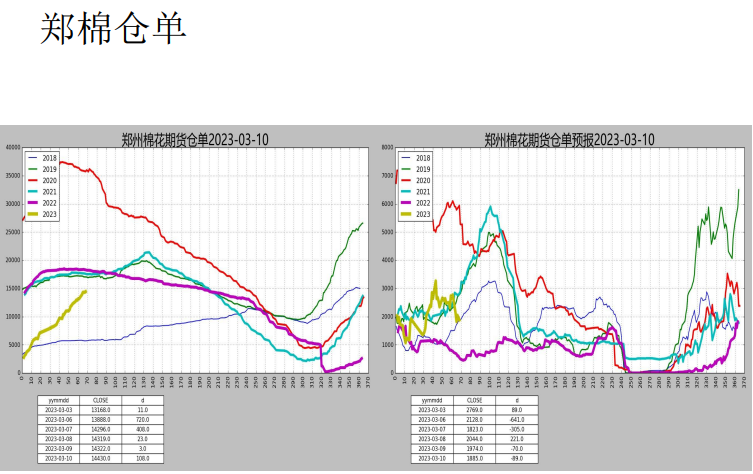

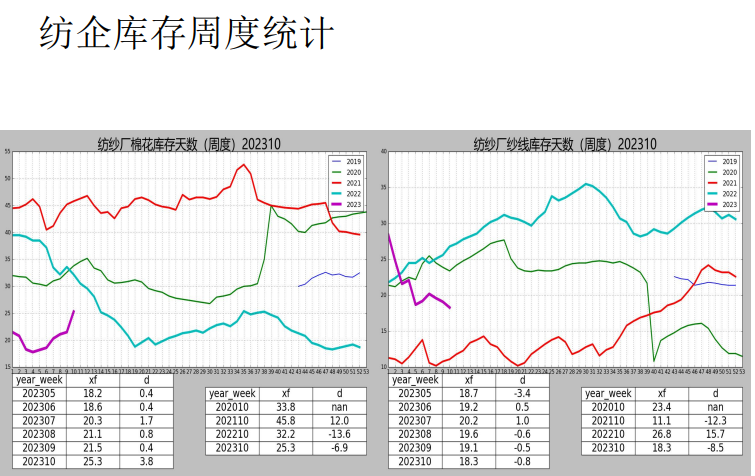

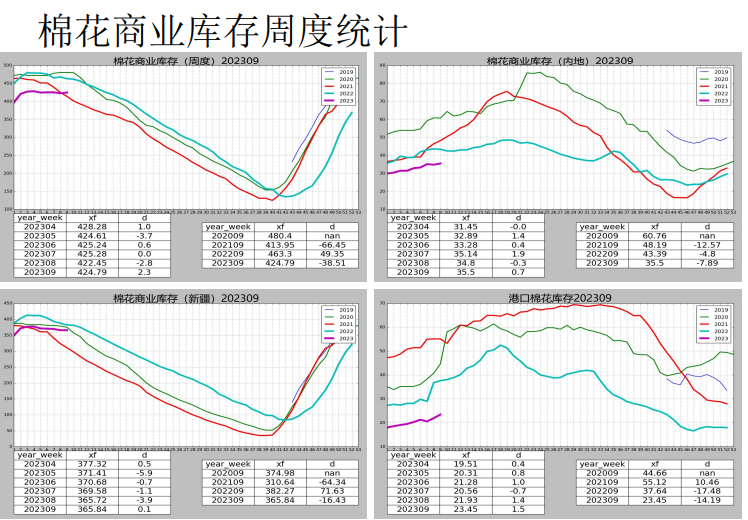

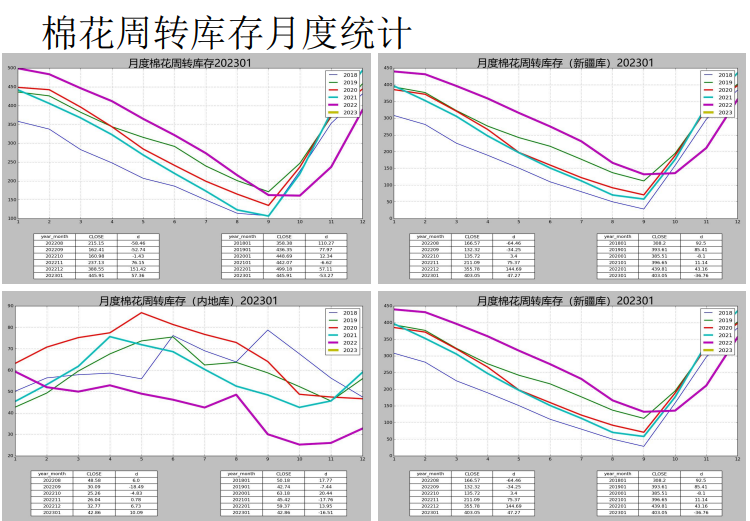

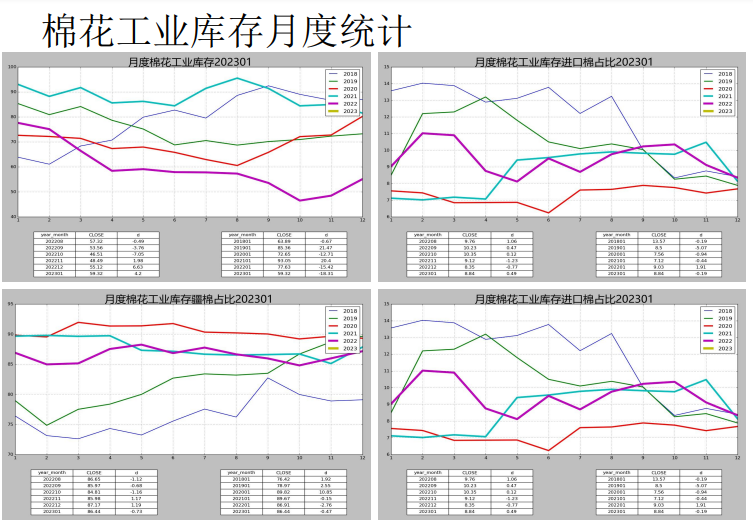

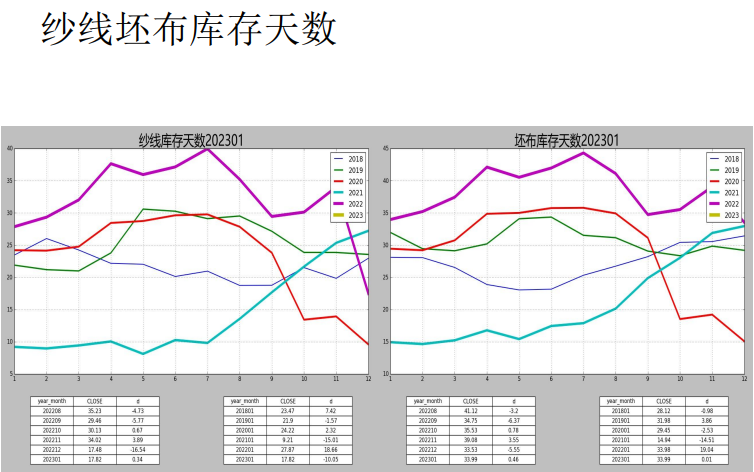

Inventory side, bonded areacottonInventories increased week-on-week, and national business inventories increased week-on-week. The inventory of cotton raw materials in spinning enterprises increased, and the inventory of yarn decreased week-on-week. Gray cloth inventory is high.

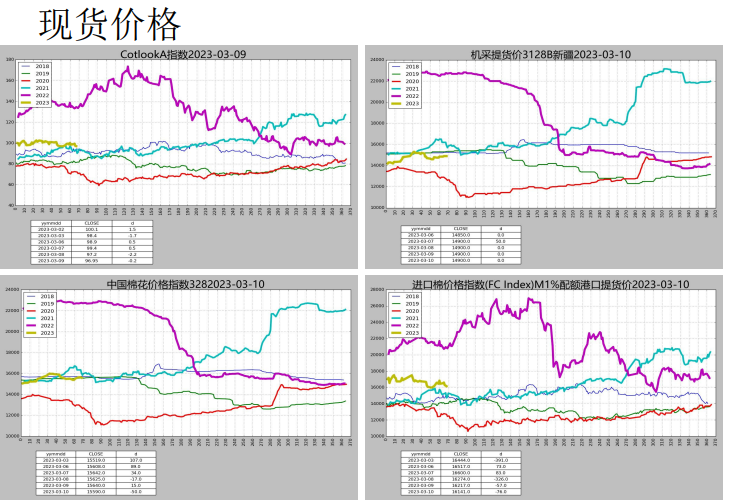

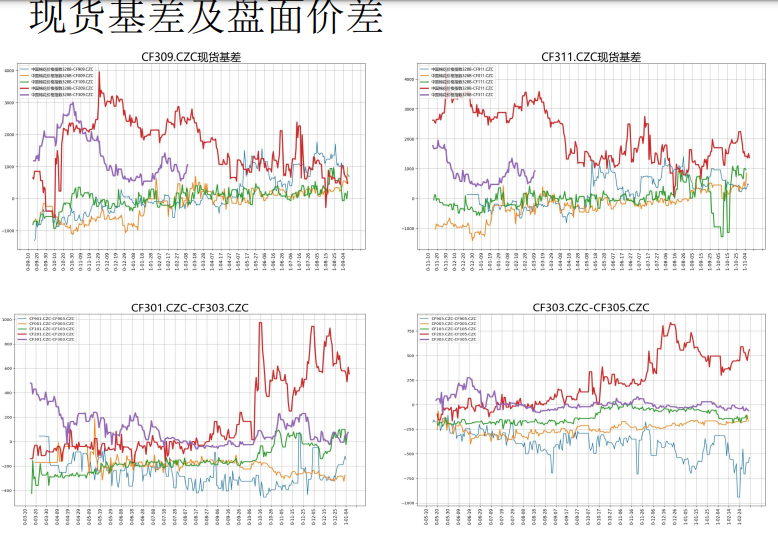

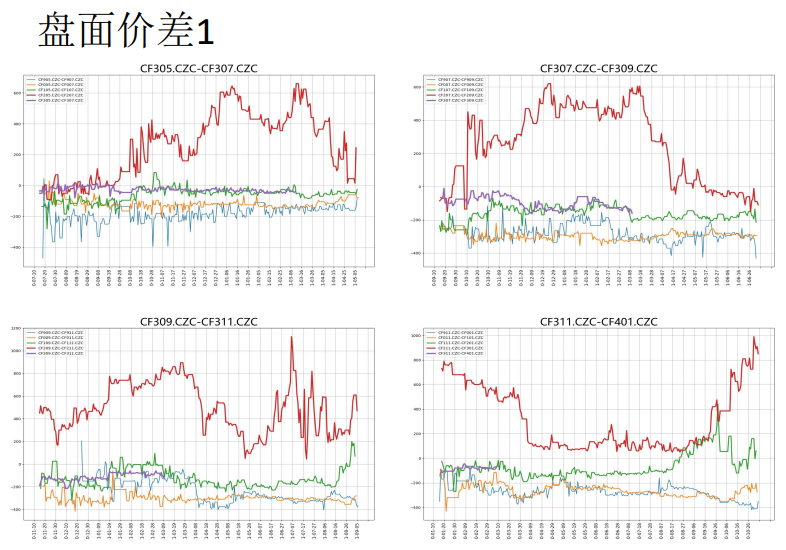

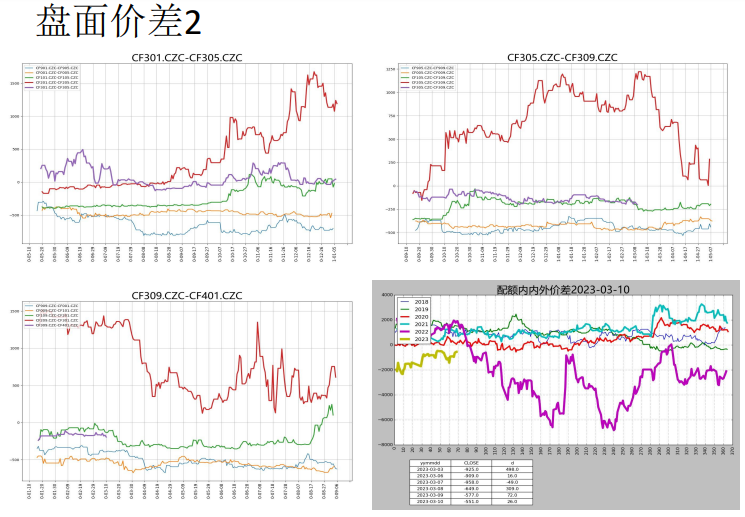

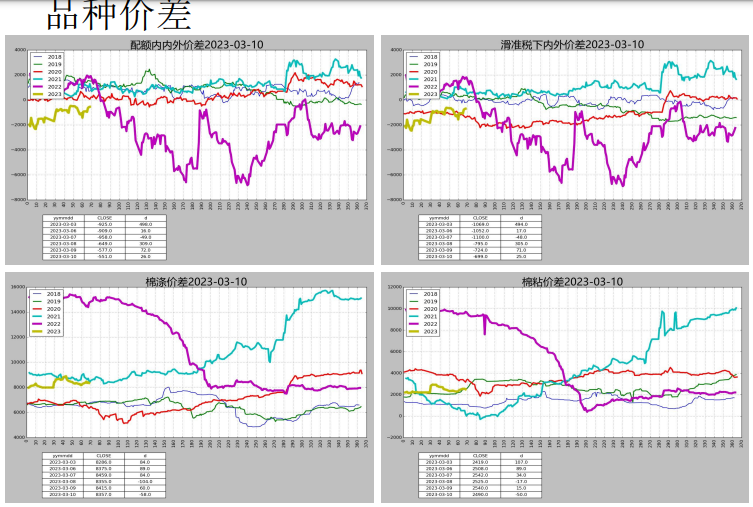

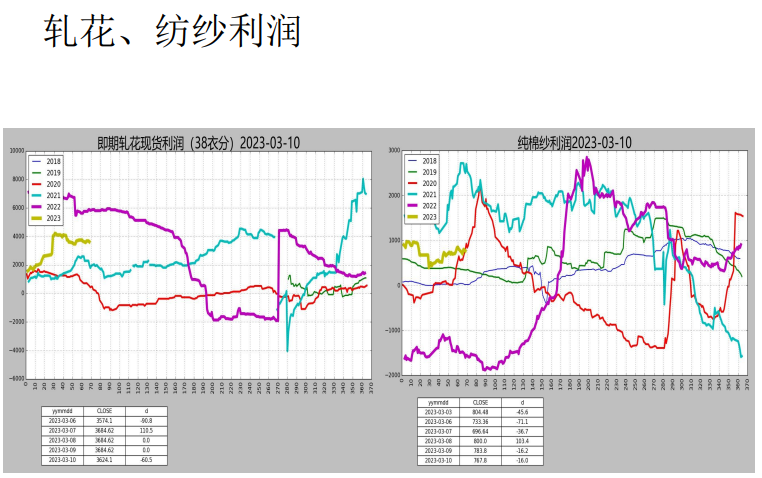

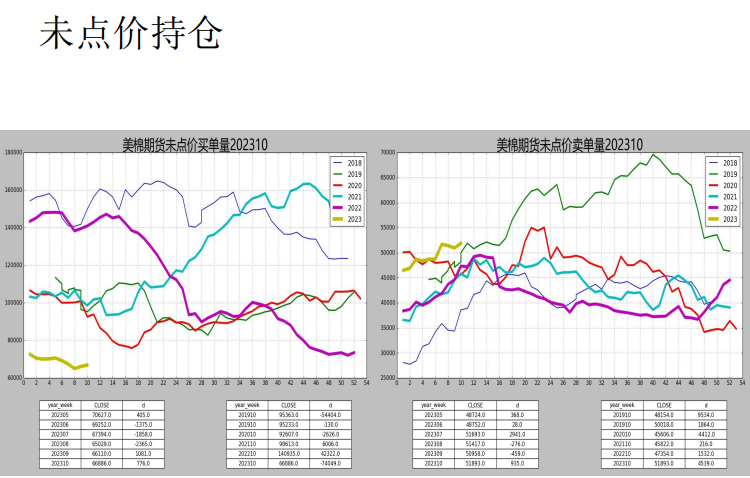

In terms of price difference, inside and outside are upside down, and the price difference is narrowed by the outside drop. The profit of spot pure cotton yarn increased slightly.

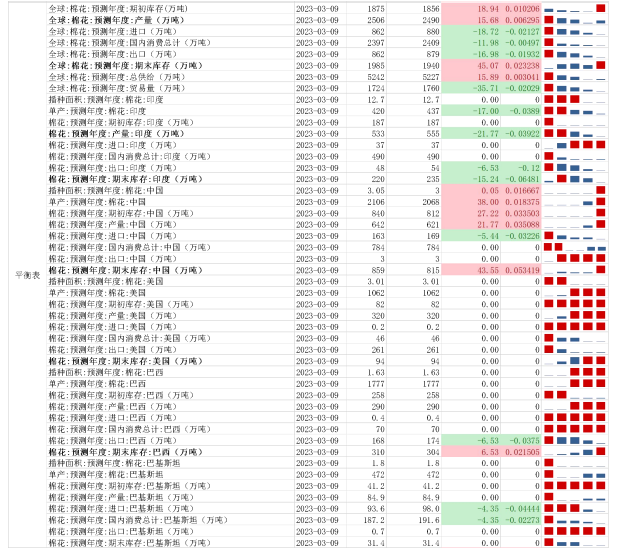

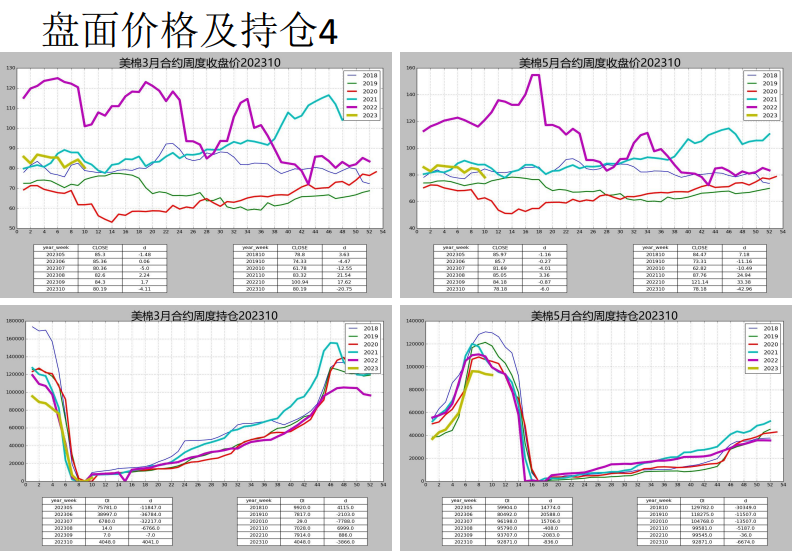

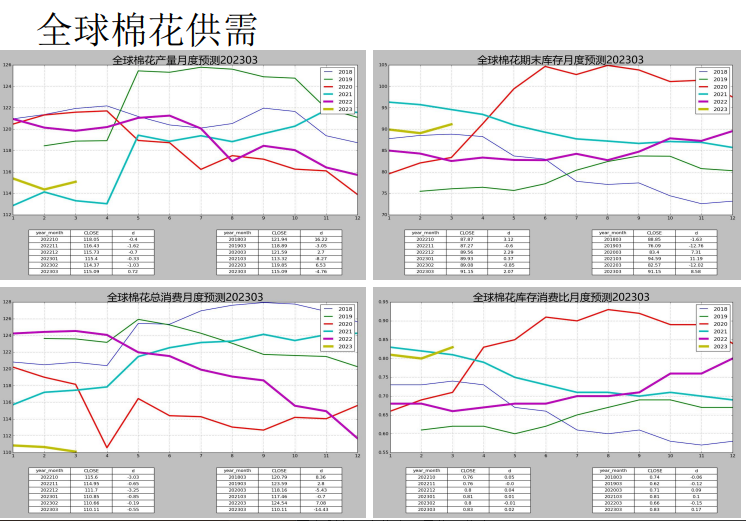

[February USDA supply and demand report is bearish]

The initial inventory increased by 190,000 tons, the output increased by 157,000 tons month-on-month, the consumption decreased by 120,000 tons month-on-month, the ending inventory increased by 450,000 tons month-on-month, and the inventory sales increased month-on-month. Supply is greater than demand, bearish.

Specifically, China has significantly increased its initial inventory. Increases in China and Australia more than offset a reduction in India. The reductions in consumption are mainly in Indonesia, Pakistan, Bangladesh, and Turkey, reflecting weaker demand in Europe and the United States. China’s beginning inventory and production increased, consumption was not adjusted, and ending inventory increased. The domestic balance sheet reflects the bearish side.

【Summary and Operation Suggestions】

On the supply side, the acreage in China and the United States is expected to decrease. On the demand side, US cotton sales slowed down. Domestic new cotton sales have a slightly limited marginal increase. Downstream boot highs increased.

In terms of inventory, the inventory of downstream cotton raw materials has risen from a low level, the inventory of yarn has declined, and the inventory of gray cloth is still at a high level. The market weakened, and the bulls withdrew from the sidelines.

In the long run, the valuation of cotton is neutral and low. There is no real positive driver on the supply side, and the margin on the demand side is weakening.

Sina Statement: This news is reproduced from Sina’s cooperative media. Sina.com publishes this article for the purpose of conveying more information, which does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Massive information, accurate interpretation, all in the Sina Finance APP