Research report text

As for U.S. soybeans, the expectations of Argentina’s production cuts and Brazil’s slow harvest continue to strengthen, and the extent to which U.S. soybean export demand will be squeezed in the short term awaits market verification. The domestic crushing profit in the United States remained stable, which supported the price center of the US soybean, and the short-term shock of the US soybean was weak.

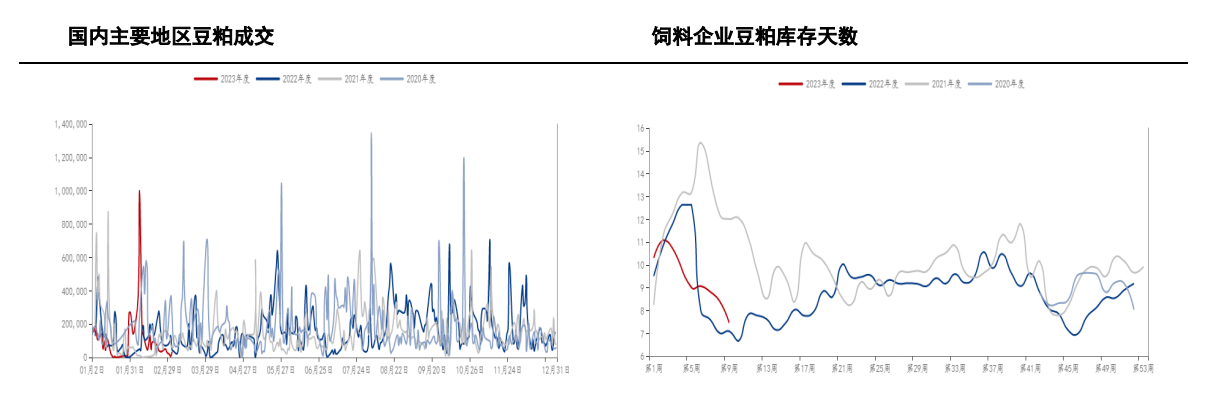

On the domestic front, the downstream demand is weak, feed companies are not willing to accumulate inventory, and the start-up of oil plants has declined.soybean mealThere is a certain pressure on inventory, and the spot is weak.but marchsoybeanThe arrival in Hong Kong is not expected enough, and the inventory of feed companies has gradually declined to a low level. Even soybean meal may remain volatile in the near future.

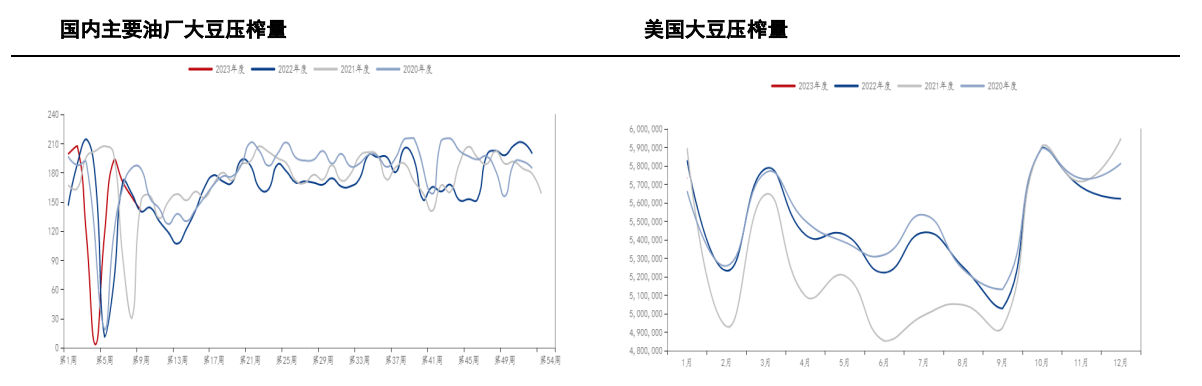

According to relevant data, in the eighth week (February 18 to February 24), the actual soybean crushing volume of 111 oil factories was 1.5477 million tons, and the operating rate was 52.01%.

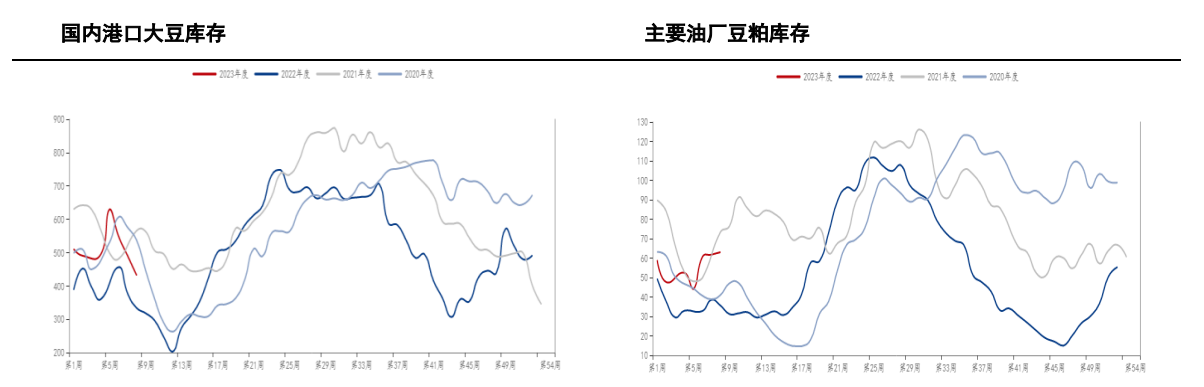

In the eighth week of 2023, the soybean inventory of major oil factories across the country continued to decline, while the soybean meal inventory continued to rise. Among them, the soybean inventory was 3.3242 million tons, a decrease of 450,200 tons or 11.93% compared with last week, and an increase of 653,900 tons or 24.49% year-on-year. The soybean meal inventory was 630,100 tons, an increase of 12,600 tons or 2.04% from last week, and an increase of 273,900 tons or 76.9% year-on-year.

According to agency surveys, Brazil’s 2022/23 soybean harvest rate is 39.7%, far lower than the 50.5% in the same period last year. Brazil’s soybean production is expected to be 152.43 million tons in 2022/2023, compared with the previous forecast of 153.37 million tons.

Buxar: As of March 2, Argentina’s soybean crop status rating was 67% poor (60% last week, 23% last year); generally 31% (37% last week, 50% last year); excellent 2 % (3% last week, 27% last year). 74% of the soil moisture is in short to extreme shortage (71% last week, 32% last year); 26% is beneficial to suitable (29% last week, 67% last year).

It is reported that India in FebruarypalmOil imports slumped 30 percent from the previous month, hitting an eight-month low, as refiners opted to reduce inventory levels as heavy imports filled inventories during the October-January period. India’s palm oil imports fell to 586,000 tonnes in February, the lowest since June 2022, according to the average forecast of five traders. Soybean oil imports in February fell 7.3% from January to 340,000 tons; sunflower oil imports fell 67% from January’s record high to 150,000 tons.

Brazil exported 5.1999 million tons of soybeans in February, a year-on-year decrease of 17%, with an average daily export volume of 288,900 tons, a decrease of 12% from the average daily export volume of 330,100 tons in February last year. The export volume in February last year was 6.2713 million tons.

The U.S. soybean crush for January was 5.73 million short tons, or 191.1 million bushels, up from 5.62 million short tons (187 million bushels) in December.

As of last Thursday, Brazil’s 2022/23 soybean area harvested accounted for 33% of the total planted area, compared with 25% last week and 43% at the same time last year. Brazil’s soybean production is expected to be 150.9 million tons this year.

Sina Statement: This news is reproduced from Sina’s cooperative media. Sina.com publishes this article for the purpose of conveying more information, which does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Massive information, accurate interpretation, all in the Sina Finance APP