The UK’s GDP in the first quarter was in line with expectations, and the Bank of England revised up its economic and inflation forecasts.On May 12, local time, the UK’s GDP in the first quarter was 0.2% year-on-year and 0.1% quarter-on-quarter, basically in line with market expectations. Although the quarter-on-quarter recovery of household consumption slowed down, government consumption decreased, inventory decreased, and the trade deficit was still large, the latest data showed In 2023, with the fall of natural gas prices, the UK trade deficit has begun to narrow, and the superimposed job market is still relatively healthy, and the risk of UK economic recession has eased. At the May monetary policy meeting, the Bank of England decided to raise interest rates by 25BP to 4.5%. At the same time, based on the improvement of energy prices and the resilience of the global economy (China’s economic recovery and the health of the US labor market), the Bank of England has significantly revised its economic forecast. It is expected that in 2023 Real GDP grew by 0.25% (February forecast -0.5%), but the CPI inflation forecast has also been revised up sharply. 23Q4 will only fall back to 5.1%, and it is expected to fall back to 2% in 2025.

But the British economy is weaker among developed countries, and the long-term downturn has not improved.1) The post-epidemic recovery of the British economy lags far behind overseas developed economies. It can be seen from the above part that the upward revision of the Bank of England’s forecast for the UK economy is mainly based on external factors, such as energy prices and the improvement of the overseas economy, rather than the improvement of the internal momentum of the UK economy. There are signs of weakening, household consumption is weakening, and at the same time, Brexit has caused a blow to the competitiveness of the manufacturing industry, exports have weakened sharply, and the trade deficit has expanded sharply. It is the sudden arrival of the epidemic that temporarily halted this process. Since 2022, the outbreak of the Russia-Ukraine conflict has caused global energy and food prices to soar, which has directly led to a substantial expansion of British imports, causing the trade deficit to expand to an unprecedented level. In addition to the political turmoil in the second half of 2022, the former Prime Minister Truss launched a tax cut plan with a scale of up to 45 billion pounds immediately after taking office, triggering market concerns about the sustainability of the British government’s debt and the pension crisis, causing the exchange rate of the pound to weaken sharply , British government bond interest rates have soared. Many factors have led to the fact that, from the perspective of developed countries, the recovery of the British economy since the epidemic has been full of twists and turns, and it is relatively lagging behind the United States and Europe. 2) In the long run, the sluggish investment situation in the UK is unlikely to change. In our report last year, “Can the UK’s new tax cut plan repeat the success of the “Reagan tax cut”? – Global Macro Weekly No. 86″ (2022.09.25), we have analyzed in detail the long-term low level of investment in the UK. The long-term improvement in productivity in the UK has been slow. At the end of 2022, the former British Prime Minister’s large-scale tax cut plan intended to boost investment has proved unfeasible, and it will be even more difficult to improve this problem in the future.

Inflation in the UK remains high, and a rate hike in June may still be possible.In terms of inflation, the current CPI inflation level in the UK is still as high as 10.1%, of which food and energy prices are the main driving forces. This part will indeed improve as high-frequency prices fall, but what is more important is the UK core CPI excluding energy and food. The year-on-year rate is currently as high as 6.2%. On the one hand, this is related to the long-term low productivity in the UK. On the other hand, it is mainly due to the tight job market in the UK and high job vacancies. This is similar to that in the United States, which means that the rate of decline in core inflation in the UK may be relatively slow. Slowly, this also made the Bank of England’s statement on raising interest rates by 25BP in May and the upward revision of CPI inflation obviously biased towards “hawks”, pointing to the possibility of raising interest rates in June.

In summary, the recovery of the British economy in 2023 is slightly better than the Bank of England’s previous expectations, but mainly due to the improvement of external factors, and the long-term investment downturn is difficult to change. Even if the Bank of England’s guidance on interest rate hikes is still hawkish, it may It is difficult to make the pound appreciate sharply against the dollar this year.

Developed economy tracker: U.S. CPI in April was 5.0% year-on-year; global macro calendar: focus on U.S. retail sales and industrial production.

The following is the text

Hawkish BoE hikes rates, but economic outlook remains weak

1. The GDP in the first quarter of the UK was in line with expectations, and the Bank of England revised up its economic and inflation forecasts

On May 12, local time, the UK’s GDP in the first quarter was 0.2% year-on-year and 0.1% quarter-on-quarter, basically in line with market expectations. Although the quarter-on-quarter recovery of household consumption slowed down, government consumption decreased, inventory decreased, and the trade deficit was still large, the latest data showed In 2023, with the fall of natural gas prices, the UK trade deficit has begun to narrow, and the superimposed job market is still relatively healthy, and the risk of UK economic recession has eased. At the May monetary policy meeting, the Bank of England decided to raise interest rates by 25BP to 4.5%. At the same time, based on the improvement of energy prices and the resilience of the global economy (China’s economic recovery and the health of the US labor market), the Bank of England has significantly revised its economic forecast. It is expected that in 2023 Real GDP growth was 0.25% (-0.5% forecast at the February meeting), but the CPI inflation forecast was also revised up sharply. In 23Q4, it will only fall back to 5.1%, and it is expected to fall back to 2% in 2025.

2. But the British economy is weaker among developed countries, and the long-term downturn has not improved

However, the recovery of the British economy after the epidemic lags far behind overseas developed economies.It can be seen from the above part that the upward revision of the Bank of England’s forecast for the UK economy is mainly based on external factors, such as energy prices and the improvement of the overseas economy, rather than the improvement of the internal momentum of the UK economy. There are signs of weakening, household consumption is weakening, and at the same time, Brexit has caused a blow to the competitiveness of the manufacturing industry, exports have weakened sharply, and the trade deficit has expanded sharply. It is the sudden arrival of the epidemic that temporarily halted this process. Since 2022, the outbreak of the Russia-Ukraine conflict has caused global energy and food prices to soar, which has directly led to a substantial expansion of British imports, causing the trade deficit to expand to an unprecedented level. In addition to the political turmoil in the second half of 2022, the former Prime Minister Truss launched a tax cut plan with a scale of up to 45 billion pounds immediately after taking office, triggering market concerns about the sustainability of the British government’s debt and the pension crisis, causing the exchange rate of the pound to weaken sharply , British government bond interest rates have soared. Many factors have led to the fact that, from the perspective of developed countries, the recovery of the British economy since the epidemic has been full of twists and turns, and it is relatively lagging behind the United States and Europe.

In the long run, the situation of sluggish investment in the UK is unlikely to change.In our report last year, “Can the UK’s new tax cut plan repeat the success of the “Reagan tax cut”? – Global Macro Weekly No. 86″ (2022.09.25), we have analyzed in detail the problem of insufficient investment in the UK, which has led to long-term production in the UK. Efficiency is improving slowly. The large-scale tax cut plan of the former British Prime Minister aimed at boosting investment at the end of 2022 has proved unfeasible, and it will be more difficult to improve this problem in the future.

3. Inflation in the UK remains high, and interest rate hikes in June may still be possible

Inflation remains high in the UK, and a rate hike in June is still possible.In terms of inflation, the current CPI inflation level in the UK is still as high as 10.1%, of which food and energy prices are the main driving forces. This part will indeed improve as high-frequency prices fall, but what is more important is the UK core CPI excluding energy and food. The year-on-year rate is currently as high as 6.2%. On the one hand, this is related to the long-term low productivity in the UK. On the other hand, it is mainly due to the tight job market in the UK and high job vacancies. This is similar to that in the United States, which means that the rate of decline in core inflation in the UK may be relatively slow. Slowly, this also made the Bank of England’s statement on raising interest rates by 25BP in May and the upward revision of CPI inflation obviously biased towards “hawks”, pointing to the possibility of raising interest rates in June.

In summary, the recovery of the British economy in 2023 is slightly better than the Bank of England’s previous expectations, but mainly due to the improvement of external factors, and the long-term investment downturn is difficult to change. Even if the Bank of England’s guidance on interest rate hikes is still hawkish, it may It is difficult to make the pound appreciate sharply against the dollar this year.

Developed economy tracker: US CPI in April was 5.0% year-on-year

Demand: In the first quarter, the actual GDP of the UK was 0.2% year-on-year and 0.1% quarter-on-quarter, basically in line with market expectations.This week’s US Redbook retail sales index remained the same as last week.

Real Estate: This week, the US MBA Market Composite Index rose to 227.8.U.S. 30-year and 15-year mortgage rates fell to 6.35% and 5.75%, respectively, this week.

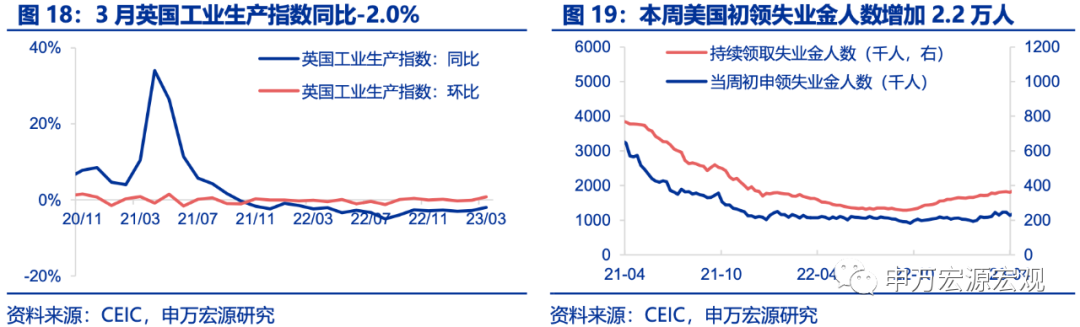

Supply and employment: In March, the German industrial output index was 1.6% year-on-year and -3.4% month-on-month, lower than expected.In March, U.S. wholesale sales were -2.9% year-on-year, and wholesale inventories were 9.1% year-on-year. In March, the UK industrial production index was -2.0% year-on-year and 0.8% month-on-month. This week, the number of Americans claiming unemployment benefits rose more than expected by 22,000.

CPI inflation:In April, Germany’s CPI was 7.2% year-on-year and 0.4% month-on-month, and inflation rose slightly. In April, the US CPI was 5.0% year-on-year and 0.4% month-on-month, in line with expectations.

Oil price and PPI: As of May 12, the weekly average price of Brent oil rose slightly to $76/barrel. In April, the U.S. PPI was 2.4% year-on-year, a record low in more than two years, and 0.2% month-on-month.

Overseas finances: In April, the US federal government’s expenditure was -16.8% year-on-year, revenue -26.1% year-on-year, and the fiscal surplus was 176.2 billion US dollars. Affected by the sharp decline in personal tax revenue, the year-on-year decline in fiscal revenue expanded by 25.5pcts from the previous month.

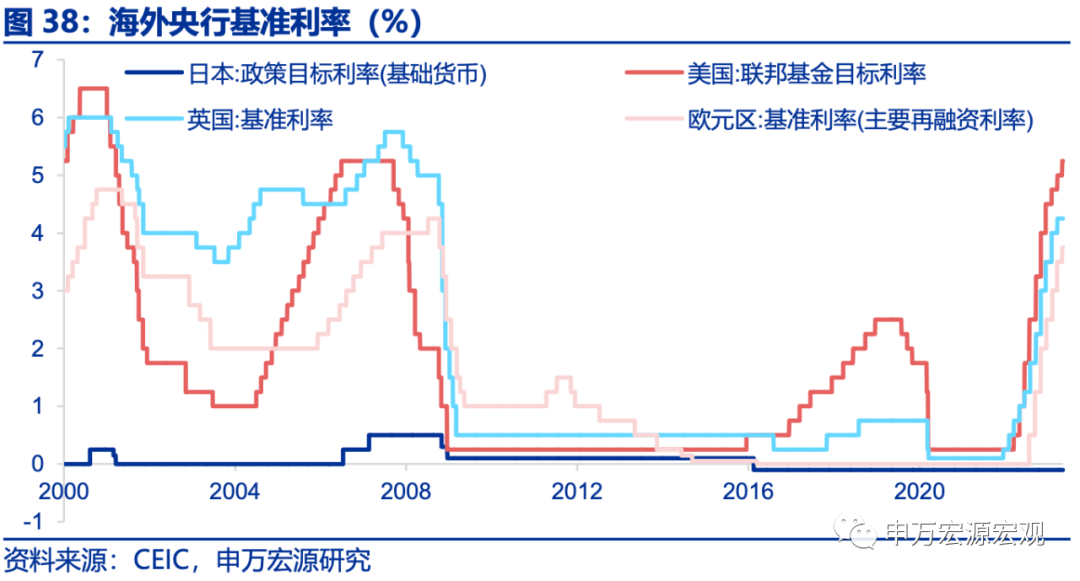

Currency operations: As of May 11, the Fed’s reverse repurchase operations averaged $2.2 trillion this week. This week, the market expects the Fed to suspend interest rate hikes in June 23 leading the probability (87.1%).

Exchange Rate Gold: As of May 12, the 10Y U.S. bond interest rate rose slightly to 3.46% from last week. The price of gold in London rose first and then fell this week. The U.S. dollar index rebounded slightly this week, rising to 102.7 as of May 12.

Emerging Market Tracker: Mexico April CPI 6.3% YoY

Unemployment and inflation data for several emerging economies will be announced this week.Unemployment rates improved in both Türkiye and South Korea. Turkey’s unemployment rate fell to 10.2% in March from 10.7% in February. South Korea’s unemployment rate also fell in April, falling back to a record low of 2.6%. In terms of inflation, Mexico’s CPI continued to decline in April, at 6.3% year-on-year and -0.02% month-on-month, which is also the lowest level since October 2021, mainly driven by the decline in food and alcoholic beverage prices.

In March, Saudi Arabia’s industrial production slowed down year-on-year, while Brazil’s industrial production rebounded year-on-year.Saudi Arabia’s industrial production rose by 4.1% year-on-year in March, slowing from the previous month. This is also the weakest data since May 2021, mainly dragged down by the manufacturing industry. Brazil’s industrial production rebounded to 0.9% year-on-year in March, of which mining and manufacturing increased by 3.3% and 0.5% year-on-year, respectively.

Overseas central bank officials say: European Central Bank hints at further interest rate hikes

Overseas central bank trends: the total assets of the Federal Reserve have declined

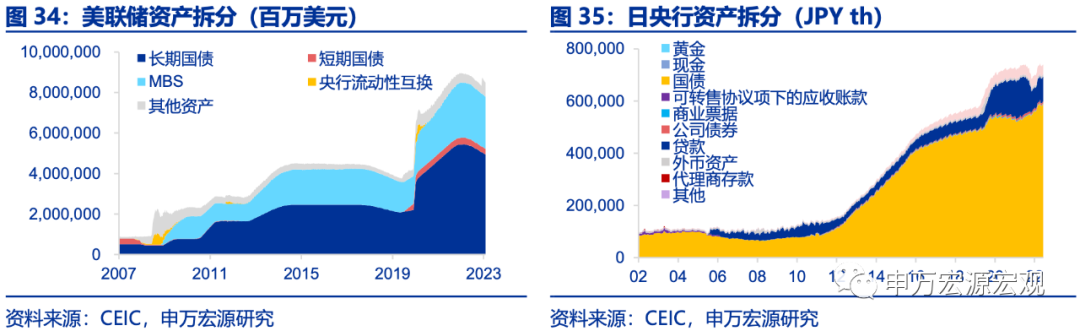

As of May 10, the total assets of the Federal Reserve fell by US$980 million from last week.As of May 5, the total assets of the ECB decreased by 2.9 billion euros compared with last week. As of May 10, the total assets of the Bank of Japan were 739.9 trillion yen, a decrease of 158.6 billion yen from last week. As of May 10, the total assets of the Bank of England were 1.03 trillion pounds, a decrease of 1.24 billion pounds from the previous period.

Global macro calendar: Watch U.S. retail sales, industrial production

This article is selected from the WeChat public account:Shenwan Hongyuanmacro. author:Wang Maoyu. Zhitong Finance Editor: Zhang Jiwei.

Massive information, accurate interpretation, all in the Sina Finance APP