image source,Getty Images

During the epidemic, China’s exports were hit first, then climbed to the peak, and then fell to the bottom, experiencing a “roller coaster”.

From December 15th to 16th, China holds the Central Economic Work Conference. This meeting at the end of December every year reveals the keynote of economic policies for the coming year, including finance, currency, and even the latest trends in important industries such as real estate, the Internet, and automobiles. The market is watching.

There are two special backgrounds for this meeting: the four members of the Standing Committee of the Politburo (Li Qiang, Cai Qi, Ding Xuexiang, and Li Xi) who emerged after the “Twentieth National Congress” of the Communist Party of China in October attended the meeting. The admiral confirmed China’s new chief economic officer, so this is a meeting where the old and the new are handing over. At the end of November, China suddenly relaxed strict epidemic prevention and control, which brought hope to the current economy that is currently mired in the quagmire. Next year, the economy will face a new era. environment of.

This meeting gave “stable growth” the highest priority, changing the situation where “stable employment” was ranked first, and did not mention “clearing”, but said “better coordinate epidemic prevention and control and economic and social development.” In addition, the statement of “increasing macro-policy regulation and control” has been added. Many economists believe that this means that there will be a larger-scale stimulus to economic recovery next year.

In terms of specific industries, housing improvement, new energy vehicles, and elderly care services were specifically mentioned to boost domestic demand; support for the development of platform companies was also discussed. Among these four industries, real estate and platform companies (Alibaba, Tencent, Meituan, etc.) have been squeezed by strict regulations and economic deterioration in the past few years, and analysts expect them to “take a breather” in 2023.

How is China’s economy?

The official judgment given by the meeting is-“The current foundation for my country’s economic recovery is not yet solid, the triple pressure of demand contraction, supply shock, and weakening expectations is still relatively large, and the external environment is turbulent, which has deepened the impact on my country’s economy.”

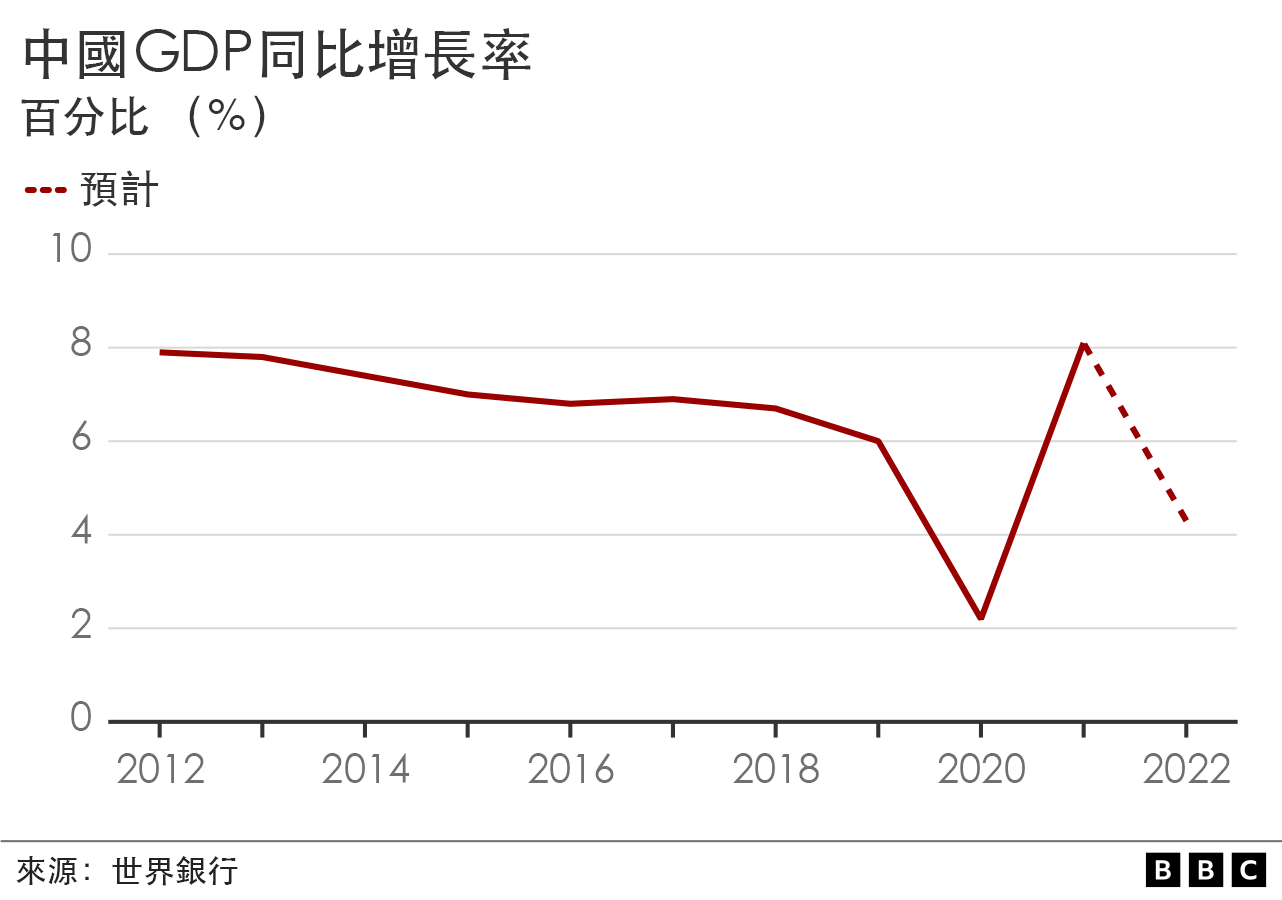

Judging from the data, the Chinese economy has gone on a “roller coaster” during the epidemic and is currently at a trough.

The Chinese economy was hit hard at the beginning of the epidemic, but it was quickly brought under control. China’s strict epidemic prevention measures have enabled the supply chain to show strong stability during the epidemic. At the same time, the Chinese government tilts its business and credit policies towards the manufacturing industry to fill in the weaknesses and shortcomings in the industrial chain in an attempt to maintain and improve the level of manufacturing. These reasons make multinational companies make decisions that are in their best interests—letting orders return to China, which has fully resumed work. In other words, since China’s supply capacity was much higher than that of foreign countries at that time, exports had an obvious substitution effect.

As a result, in the second half of 2020, China’s foreign trade stopped falling and turned to rising, and even in December 2020, China’s exports in US dollar terms increased by 18.1% year-on-year, far exceeding expectations. On the basis of such high growth, China’s foreign trade will continue to advance at a high speed in 2021-the annual export will be 21.73 trillion yuan, an increase of 21.2%. So far, China’s trade volume has grown positively for six consecutive quarters, and its share in the world has even reached a historical peak.

At the beginning of this year, the second reversal occurred. Omicron attacked China, and large, medium and small cities were closed one after another. Unlike the “short-term pain” at the beginning of the epidemic, the Chinese economy will experience “labor pains” in 2022, which will last throughout the year. Economic growth nearly stalled in the second quarter and for the full year is estimated at 3%, missing the 5.5% target.

Data released in November showed that China’s exports shrank for the first time after 29 months of growth; the total retail sales of consumer goods in November was 3,861.5 billion yuan, a year-on-year decrease of 5.9%. Hong Hao, chief economist of Cirrus Investment Group, believes that this means that China’s internal and external demand is simultaneously fading.

Xu Tianchen, an economic analyst at the Economist Intelligence Unit (EIU), told BBC Chinese that economic recovery first and foremost depends on China’s reopening. A smooth transition to “living with the virus” would certainly boost confidence, spending and investment, but it’s not yet a certainty. Supportive policies could inject further impetus into the economy, but are unlikely to be game-changing.

“Officials in China are clearly very concerned about fiscal sustainability, as the phrase ‘local government debt risk’ appears an unusual three times in the meeting statement. I note that they dropped the reference to ‘tax cuts’ in the document, This further shows that they don’t want to stretch the government’s finances too tightly,” Xu Tianchen said.

image source,Getty Images

By the end of 2022, after the epidemic prevention policy is relaxed, how will it recover? (Pictured: A woman chooses traditional red lanterns at a market in preparation for decorating her home during the Lunar New Year).

Stimulate domestic demand and expand income

There’s an old joke among economists – “Just teach a parrot to say ‘supply’ and ‘demand,’ and it’ll be called an economist.”

At the beginning of the epidemic, the Chinese economy faced a rare situation where both sides of “supply” and “demand” were simultaneously frozen. On the supply side, factories stop working and production, and goods stop shipping; on the demand side, ordinary people stay at home and stop shopping, having dinners, traveling and watching movies.

From the second quarter of 2020 to the end of 2021, both “supply” and “demand” have been restored, and “demand” has recovered more slowly, and ordinary people are still cautiously consuming in the face of uncertainty; while factories on the “supply side” rely on Overseas orders even surpassed before the epidemic, from bicycles, fitness equipment, to electronic products, production and export at full capacity.

By 2022, China will once again face a situation where both “supply” and “demand” are in trouble at the same time. On the supply side, Europe and the United States are gradually unblocking, and orders are returning to other manufacturing centers. The Fed’s interest rate hike has suppressed external demand, and the epidemic prevention policy has interrupted production and transportation. ; The setback on the demand side is more direct. The successive city closures and income reductions have caused residents to either reduce additional consumption, or stay at home with nowhere to spend money.

By the end of 2022, after the epidemic prevention policy is relaxed, how will it recover? The above-mentioned Central Economic Work Conference, when arranging economic work in 2023, ranked “expanding domestic demand” as the first priority, and emphasized that “we must fully tap the potential of the domestic market and enhance the role of domestic demand in stimulating economic growth.”

Specifically, it is to give priority to the recovery and expansion of consumption, “enhance consumption capacity, improve consumption conditions, and innovate consumption scenarios.” It seems logical to do so. With the reduction of overseas orders, stimulating domestic consumption will not only boost demand, but also stimulate the recovery of the supply side.

image source,Getty Image

On December 6, the epidemic prevention policy was suddenly relaxed, and there was only one customer dining in an empty restaurant in Beijing.

However, Ren Zeping, a Chinese economist, reminded that consumption is affected by factors such as consumption capacity, willingness to consume, and consumption scenarios. The slow recovery of consumption is limited to a certain extent by residents’ income and employment. There are still structural problems in current employment.

China’s urban surveyed unemployment rate in November was 5.7%, which continued to rise compared with October, and the surveyed unemployment rate of the population aged 16-24 was still at a double-digit high. Based on this, Ren Zeping suggested that the government issue consumer vouchers, which will help open up the national economic cycle, help some people in need to overcome temporary difficulties, and boost public confidence. The source of funds can be through special government bonds.

It is worth mentioning that on December 14, China announced the “Strategic Planning Outline for Expanding Domestic Demand (2022-2035)”, stating that it is necessary to firmly implement the strategy of expanding domestic demand, continuously release the potential of domestic demand, and give full play to the role of stimulating domestic demand.

China’s eastern neighbor Japan once formulated a similar plan, namely the “National Income Doubling Plan” from 1961 to 1970. The difference is that the plan anchored the economic development goal on the “national income” indicator; similarly, income After doubling, domestic demand can be greatly released, bringing surging impetus to economic growth. This plan has achieved great success. Japan’s per capita national income increased from US$395 in 1960 to US$1,592 in 1970, surpassing France and Germany successively, and ranking second in the world after the United States.

Which industries are likely to benefit?

Xu Tianchen said, “Two things impressed me about the meeting: the persistence in promoting consumption, and the retreat in the regulation that is destructive to technology companies. This pro-growth stance, as well as the reversal of some early policies, clearly It clearly reflects Chinese leaders’ concerns about the economic scars from the ‘zeroing out’ policy.”

In the item of “expanding domestic demand”, only three industries were named in the meeting draft: “supporting housing improvement, new energy vehicles, elderly care services and other consumption”.

Among them, new energy vehicles are one of the industries with the most significant development among the 10 fields selected by “Made in China 2025”. Through subsidies and other methods, the sales volume has increased from 12,000 to 3.52 million in 10 years. China hopes to change from a follower of Germany, the United States and Japan to overtaking at corners and become a leader in the process of great changes in the auto industry. Economist Intelligence Unit (EIU) analyst Arushi Kotecha (Arushi Kotecha) said that electric vehicles remain crucial to economic growth, partly because of its significance and key role in the energy transition; It is a high value-added part of an economy because it includes not only the latest technologies in the lithium-ion battery and semiconductor fields, but also the vehicle driver assistance component industry (such as lidar).

image source,Getty Images

Electric cars of Chinese brands at the Shanghai Auto Show in 2020.

Behind the elderly care service is another problem facing China, “aging”. The birth rate in China has dropped again and again during the three years of the epidemic, putting the “only child” generation under enormous pressure. Traditionally, the elderly in China tend to live at home, which makes the institutions and services for the elderly underdeveloped.

However, compared with the former two, real estate is much more important to the Chinese economy. The upstream of real estate includes building materials, chemicals, steel, construction machinery, and downstream home appliances, furniture, decoration, etc., involving many industries and becoming the key to stimulating domestic demand in China. However, in 2020, China proposed “three red lines” for the financing of key real estate companies, and proposed restrictions on real estate loans to financial institutions. Within a few months, more than 100 real estate companies operating with high leverage have defaulted on their bonds and their capital chains have broken. They even closed down, and “unfinished buildings” appeared in batches. By 2022, buyers of hundreds of real estate properties have signed a joint statement online, announcing that if the “unfinished buildings” do not resume work, they will no longer pay loans.

In the midst of the economic downturn and the dilemma of “unfinished buildings”, the Chinese government’s policies have been shifting, and more and more restrictions on the property market have been relaxed. On December 15, Chinese Vice Premier Liu He said, “Real estate is a pillar industry of the national economy. In response to the current downside risks, we have introduced some policies and are considering new measures to improve the industry’s balance sheet and guide the market. Expectations and confidence are picking up.”

But Albert Park, chief economist of the Asian Development Bank (ADB), believes that the relationship between the Chinese government and real estate has not fundamentally changed—the government sells land at high prices to generate fiscal revenue and fund public investment. Further reforms are therefore needed to provide local governments with alternative sources of revenue that allow them to distance themselves from the real estate industry.

image source,Getty Images

“Unfinished building” has become a tragic footnote in the era of China’s real estate industry.

In the past few years, China’s Internet companies have had a similar fate to real estate companies. Almost without warning, from 2020 to 2021, antitrust investigations against Internet giants will kick off quite dramatically——Jack Ma “fired” on financial regulators in a public speech, and then Ant Financial was suspended on the eve of listing ; Didi went public in the United States “cut first and then play”, and was censored and removed from the shelves within a week, and was delisted in less than half a year; in addition, Ali received a huge fine of 18.2 billion, and Tencent was suspended from issuing the game version number. Afterwards, the “Wall Street Journal” reported that Xi Jinping personally stopped the listing of Ant Financial; and the “Financial Times” reported that Jack Ma had moved to Japan for half a year. Public opinion is therefore worried, whether the Chinese economy has begun to “advance the country and retreat from the people”?

The draft of the meeting said on the one hand that we must vigorously develop the digital economy; The law stipulates the requirement of equal treatment of state-owned and private enterprises, and encourages and supports the development and growth of the private economy and private enterprises in terms of policy and public opinion. Protect the property rights of private enterprises and the rights and interests of entrepreneurs in accordance with the law.

The “two unwavering” refers to “unswervingly consolidating and developing the public sector of the economy, unswervingly encouraging, supporting, and guiding the development of the non-public sector of the economy, ensuring that all types of ownership of the economy equally use production factors in accordance with the law, fairly participate in market competition, are equally protected by law.”

Analysts believe that this is “emphasis on countering the planned economy speech from public opinion and protecting private enterprises”, and this directional change is actually far more far-reaching than a specific industry policy.