Source: China Securities Construction Investment Author: China Securities Construction Investment Futures

Research report text

【Viewpoints and Strategies】

coke:

【Inventory Change】

The inventory of coke enterprises and steel mills continued to decline, and the inventory of ports continued to decline; the overall inventory continued to decline, and the coke inventory drove upward. The available days of coke inventory in steel mills continued to decline.

【Fundamentals】

The loss of steel mills has intensified, and the output of molten iron has dropped again; the number of days available for raw materials in steel mills has continued to decline at a low level. .

【expected】

Demand expectations: 1) The macro sentiment has improved, real estate benefits are frequent, the epidemic situation is gradually released, and terminal repair expectations are enhanced; 2) The losses of threaded blast furnaces have intensified, and steel mills may force the price of raw materials to drop, and then replenish the warehouse at low prices.

【Main logic】

The gross profit margin of Jiaogang rebounded to 4%, driven downward by profit;coking coalInventory drives neutral down, coke inventory drives up; based on three rounds of landing, the warehouse receipts are 2965, the J01 contract rises slightly, and the basis drives down.

【Strategy】

Neutral: The coke 05 contract has seen a large increase, and the short-term callback support refers to 2760-2785. It is recommended to call back wet positions and short positions, and the pressure is around 3000; for the medium and long-term, it is recommended to sell short on rallies.

Coking coal:

【Inventory Change】

The inventory of coal washing plants has increased, the inventory of coal mines has declined, the coking plant has accelerated inventory replenishment, the inventory of steel mills has continued to decline, and the inventory of ports has increased; the overall inventory has continued to increase, and the coking coal inventory has driven a neutral decline; the number of days available for coking coal inventory in coking plants continues to rise.

【Fundamentals】

Coal mines have not significantly increased production, mine quotations are firm, coal washing plant costs have risen, and operating rates have declined; coke companies have recovered significantly, and logistics recovery and replenishment have accelerated; the daily traffic volume of Mongolian coal at ports has risen to above 800 vehicles, and Sinotrans has gradually resumed.

【expected】

Supply expectations: 1) Shanxi’s 4.3-meter coke oven may be shut down in batches at the end of the year; 2) Most coal mines are close to completing their production capacity tasks, and may have production reduction expectations at the end of the year; 3) The increase in Mongolian coal imports is expected to further increase; 4) Australian coal will re-clear customs Worries arose.

【Main logic】

The macro-positive drivers of short trading weakened, the losses of threaded blast furnaces intensified, and Mongolian coal customs clearance vehicles continued to pick up; the margins of long trading terminals improved, and steel mills replenished warehouses before the festival with low inventory. The current industry profit pattern does not support the fourth round of increase.

【Strategy】

Neutral: The coking coal 05 contract is still strong in the short term, the JM05 pressure level is around 2000 and 2100, and the support level is 1830-1856; in the medium and long term, it is recommended to sell short on rallies; you can consider doing long 05 contracts on dips to make profits.

【1. Bifocal market information】

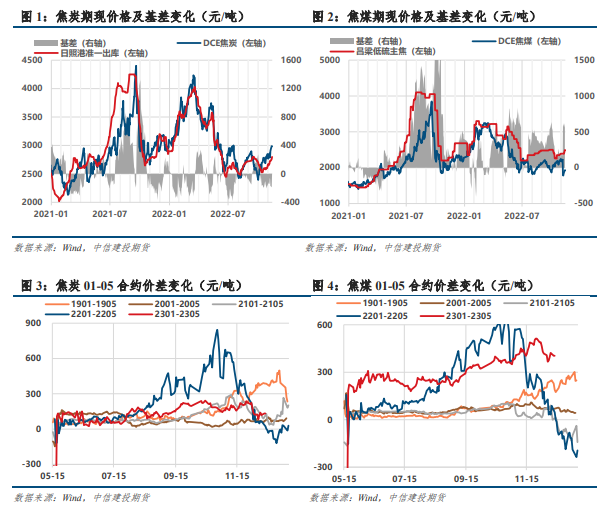

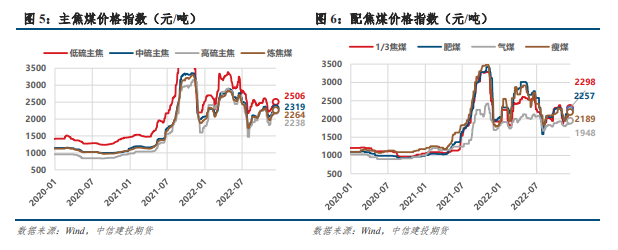

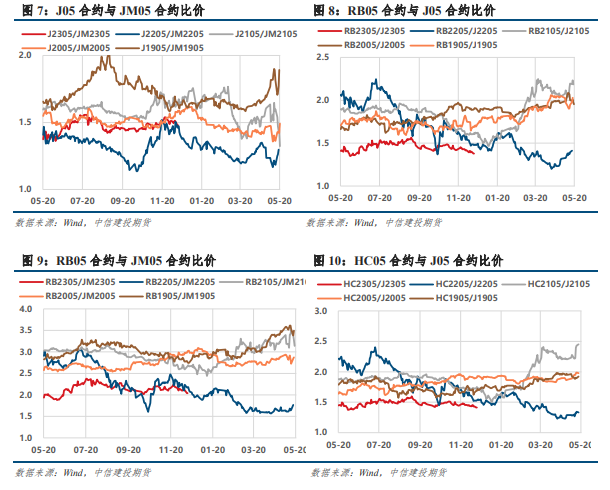

【2. Bifocal Correlation Chart】

Sina Statement: This news is reproduced from Sina’s cooperative media. Sina.com publishes this article for the purpose of conveying more information, which does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Massive information, accurate interpretation, all in the Sina Finance APP